Last updated: Jan 4, 2024

As mentioned in my previous post, Mrs. EYFI’s company ended health insurance for half-time employees starting Jan 1 of this year. So in addition to finding health insurance for her and our kids, we also needed to get dental insurance.

So, you know me: a big analysis with lots of plots ensued!

Main Questions

For this analysis I had two main questions:

1. Given our dental history (we likely won’t have any dental work beyond basic procedures such as fillings), what plan will cost the least for us?

2. Will we really save money overall by getting dental insurance, especially if there’s a cash discount?

Kids Vs Adults

A very important thing I learned as I compared plans is that kids and adults are treated very differently for dental insurance.

Typically kids and adults have different deductibles and coinsurance rates.

Adults have a max coverage amount in all dental plans I’ve seen, but if the dental insurance plan is provided via the ACA (Obamacare) marketplace, those plans are required to have a max out of pocket (OOP) for kids. For 2024, those max OOP limits are $400 for one kid and $800 for more than one kid.

If not getting an ACA plan, kiddos will have a max coverage amount just like adults (at least for all the plans I found).

When I first learned about this Max OOP for ACA plans, I was pretty excited – it seemed like a big advantage of getting dental insurance through the ACA. However, as you’ll see in the results section below, it seems like insurance companies offset this benefit by charging much higher premiums, higher deductibles, etc. It’s like these insurance companies are trying to make money off of us!

I was actually surprised to learn that you can purchase dental plans via the ACA marketplace, despite all the research I’ve done on selecting ACA health insurance. Turns out that you can’t buy an ACA dental plan unless you’re buying a health plan at the same time.

Finally, none of the plans I encountered have any kind of “family” deductible, max OOP, or max coverage. Each person has their own individual running total for these thresholds.

Initial Search For Plans

To compare plans, first you need to find the best set of viable plan options.

The most important initial step in your search is to ensure your dentist is in-network with the plan.

Or if you’re not picky about what dentist you see, you should at least confirm there are well rated dentists in your area that are in-network. Ideally though you can find a dentist that takes a variety of plans, so that if you need to change plans in the future, you’ll be able to stick with the same dentist (assuming you like them).

I recommend a couple different main approaches to find an initial set of plan options:

1. If you’re getting ACA health insurance, look at the dental plan options listed there. Make sure you plug your dentist into the application so you can see which plans they are in-network with. However, don’t fully trust those answers either – double check with the “Find a provider/dentist” tool on each insurance site, and perhaps contact your dentist office as well.

2. Check out your dentist office’s website to get a list of insurance plans they accept, and/or contact the office to get that list.

If your dentist office has a good insurance specialist, I highly recommend also talking / emailing with them about what plans and companies they have found to be the best to work with, and if any of those companies / plans have “gotchas” that trip some people up.

I had a very long and super informative email exchange with the insurance specialist at our dental office, which taught me a ton.

After you have a list of companies that might work, look at their plans to see which ones have reasonable prices to assemble your initial list of candidates for the deeper analysis.

Gather Your Info

Next up, I recommend you go back through your medical records to see how many dental procedures you had over the last few years, and what kind of procedures you had done.

Was it just cleanings, x-rays, and exams? Or did you have a handful of minor procedures like fillings? Or did you have a ton of advanced work such as crowns and bridges, etc.?

If you’re tracking your expenses as I’m always nagging you about, gathering this info should hopefully be reasonably straightforward to do.

Based on this history, and any knowledge you have about work still needed, you can estimate the likely amount and type of dental work you’ll need.

Comparison Tool

Now that you’ve gathered some candidate plans and have some idea of the type of dental work you’ll likely need, let’s see how much you’ll actually pay for a range of dental expenses.

Code

As usual, I employed Python to code up all the relevant math and build the tool.

I placed the Python code in the EYFI github repo, which you’re welcome to download and run yourself if you’d like to plug in your own values or just play around with different inputs.

When I get more time, I’ll try to place an embedded Python interpreter somewhere on this page as well, so you can run the analysis directly from here.

Inputs

Just like for the medical insurance analysis tool, there are an unfortunately large number of inputs you’ll need to fill in to run the analysis.

Fortunately most of these inputs you can find on the policy pages for each plan (and now you know what to look for).

The inputs are:

- Cash discount rate – if you don’t buy any insurance, what discount will your dentist office give you if you pay cash?

- Insurance negotiated discount rate (typically around 20%) – insurance companies negotiate with dental office to pay reduced rates, so this is the assumed discount of the full office rate for all plans (in the future I can extend this to have different discount rates for different insurance companies)

- Cash price (full office rate) for all annual preventive care for all people on policy

- Cash price (full office rate) for all annual preventive care for a child

- Cash price (full office rate) for all annual preventive care for an adult

- Annual premiums for all plans (monthly premium times 12)

- Whether the deductible is needed before the plan pays for preventive care (generally false for non-ACA plans and true for ACA plans)

- Deductible for a child for all plans

- Deductible for an adult for all plans

- Coinsurance rate for a child for all plans

- Coinsurance rate for an adult for all plans

- Max OOP for a single child for all ACA plans (set by regulation for all plans)

- Max OOP for multiple children if an ACA plan (set by regulation for all plans)

- Max coverage per person – both kids and adults if a non-ACA plan, and just adults for ACA plans

- Total number of adults to consider – used for computing base cost

- Total number of kids to consider – used for computing base cost

Just 16 inputs! So easy! But again, you should hopefully be able to get all the info just looking at the plan documents and contacting your dentist office.

Compute Base Cost For Each Plan

The base cost for each plan starts with the total annual premium. If the deductible must be paid before the plan pays for preventive work, the base cost also includes the deductible for all people on the plan (assuming the cost of the preventive work easily exceeds the deductible).

And the base cost for the “cash only” option is just the full office price of all for all annual preventive care for all people you’re including, with any cash discount.

Fun fact: Did you know that “preventive” and “preventative” mean the exact same thing? All these years I’ve been using a word that is two characters longer for absolutely no reason – crazy!

Compute Total Cost For Each Plan

Starting from the base cost, the total OOP cost for a wide range of basic service expenses are computed.

First we compute the total OOP cost for basic service expenses for a single kid.

Then we compute the total OOP cost for basic service expenses for a single adult.

The tool considers one dollar at a time, keeping running totals of money paid towards the deductible, money paid by the insurance company, and of course the total overall cost you pay.

Note 1: the cost of preventive care generally does count towards the max benefit unfortunately.

Note 2: if you do hit your max coverage amount, and thus you are responsible for paying all additional expenses, you will still get the negotiated insurance discount rate.

Note 3: many plans will not cover even basic services until a minimum amount of time has passed, such as 6 months. And some plans even improve the policy values after the first year to encourage people to stick with them over a longer period of time.

Example Scenario

Now let’s look at some actual numbers! And get some beautiful plots going!

Below are six of the best dental plans that I found when doing our search. Our dentist is in-network with all of these plans, and they offered the most reasonable prices during my initial search.

The options are a plan from MetLife, two plans from UnitedHealthCare, and three plans from from Guardian. The MetLife plan and first UHC plan are not ACA plans, and the second UHC plan and all Guardian plans are ACA plans.

Of course you will almost certainly find different initial plans for your situation, but these plans offer a nice diversity of results for illustrative purposes. And I’m lazy, so I don’t have to come up with any other numbers this way 🙂

Inputs

Inputs that are not tied to each insurance plan include:

- Cash discount rate: 10% (what our dentist offers)

- Insurance negotiated discount rate: 20% (most common from what I could tell)

- Total office rate for all standard preventive services (typically one cleaning + exam, and one cleaning + exam + x-rays), for a child: $146 + $201 = $347

- Total office rate for all standard preventive services (typically one cleaning + exam, and one cleaning + exam + x-rays), for an adult: $172 + $201 = $373

- Number of adults on plan: 1

- Number of children on plan: 2

- Total office rate for all preventive services for all people: $373 + 2*$347 = $1067

Inputs that ARE tied to each plan are:

| MetLife | UHC 1 | UHC 2 | G 1 | G 2 | G 3 | |

| Annual Premium | $723.84 | $805.56 | $867.72 | $813.36 | $842.16 | $880.2 |

| Deductible needed for preventive | No | No | Yes | Yes | Yes | Yes |

| Child Deductible | $75 | $50 | $60 | $150 | $150 | $150 |

| Adult Deductible | $75 | $50 | $50 | $50 | $50 | $50 |

| Child Coinsurance | 50% | 50% | 40% | 20% | 20% | 20% |

| Adult Coinsurance | 50% | 50% | 40% | 50% | 40% | 50% |

| Max OOP for single child | N/A | N/A | $400 | $400 | $400 | $400 |

| Max OOP for multiple children | N/A | N/A | $800 | $800 | $800 | $800 |

| Adult Max Coverage | $750 | $1000 | $1000 | $1000 | $1500 | $1000 |

| Child Max Coverage | $750 | $1000 | N/A | N/A | N/A | N/A |

Results

With all the above inputs, let’s take a look at the total OOP cost for a wide range of basic service expenses.

Note that the expenses, as shown on the x-axis, are the full office rate amounts. Nominally you will never pay these rates (you’ll likely have either a cash discount or the negotiated insurance discount), but it’s important to use the full office rate prices for a consistent comparison of the cash-only vs insurance options.

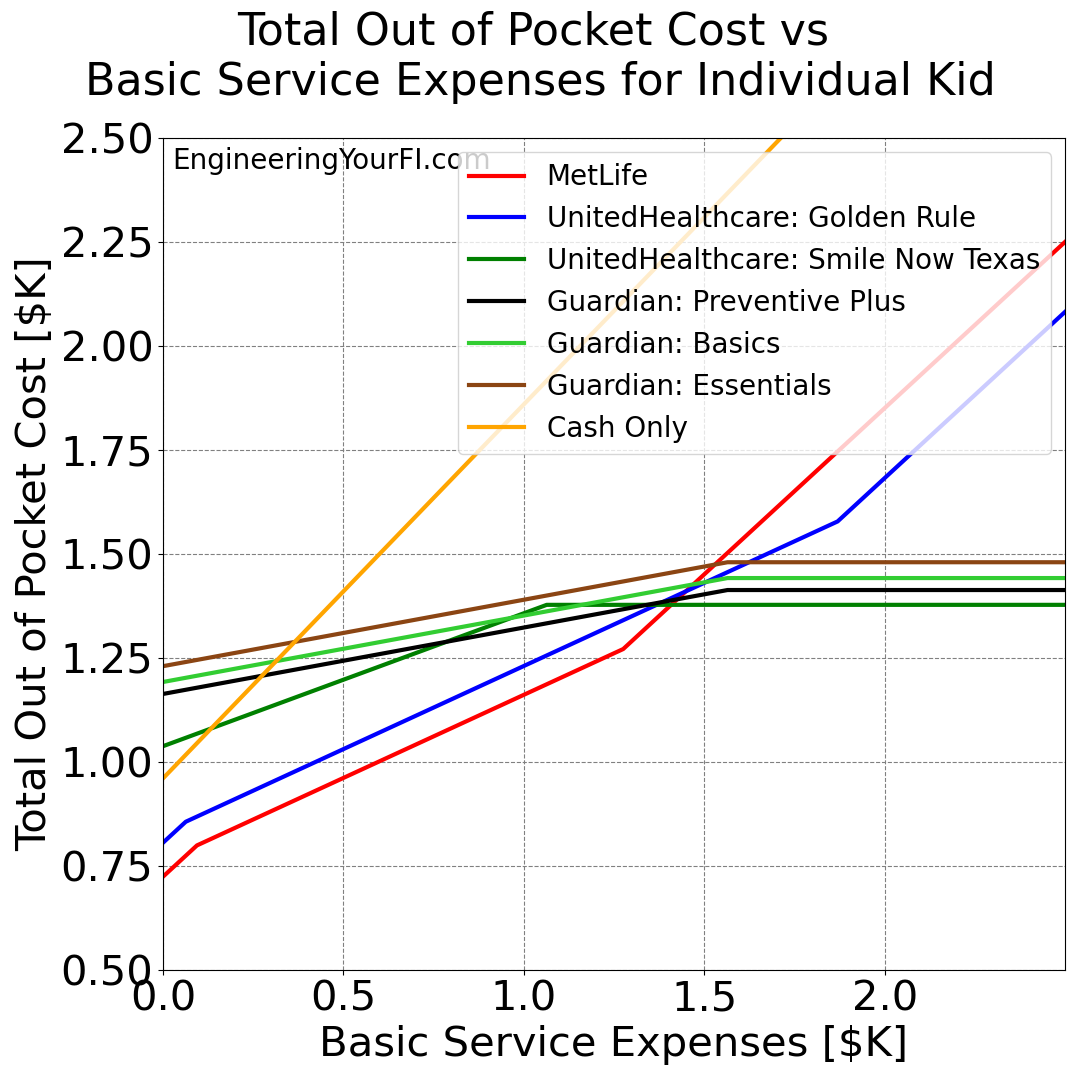

The total OOP cost for a range of basic service expenses for a single kid within a family of 1 adult and two kids is:

You can see how for basic service expenses less than about $1400, MetLife is the clear winner. If you spend more than $1400 (that’s a lot of cavities!), the second UHC plan via ACA is the winner due to that max OOP.

Note how the max OOP for all the ACA plans is much higher than $400, because we’re including the cost of the premiums and the base costs for other members of the family (assuming they just need preventive work).

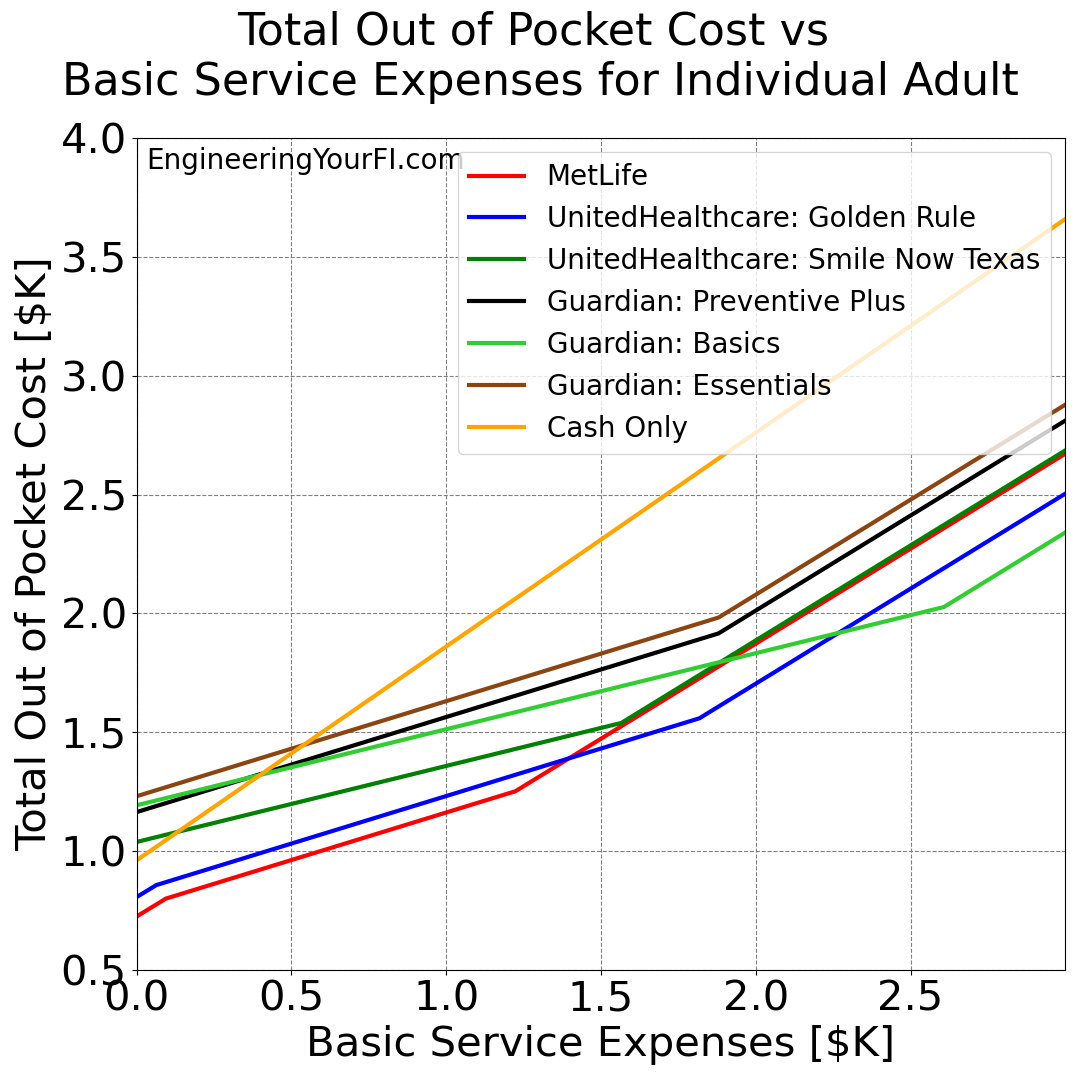

Next let’s take a look at the total OOP cost for a range of basic service expenses for a single adult in that same family:

Again MetLife is the winner if you have less than about $1400 of basic service expenses. Then the first UHC plan wins until about $2250 of expenses, and then the Guardian Basics plan wins.

These plots reveal how challenging it is to figure out the most affordable plan by just staring at all the policy parameters. You really need to plot out the total cost incorporating all those factors to be able to see clearly the winners. Well, at least I do!

What we chose for 2024: MetLife

We have no expected dental costs for 2024 except for preventive care, as that is nearly always the only dental costs we have each year. Thus we expect MetLife to be the overall cheapest option.

Conclusions

While picking a dental insurance plan is simpler than picking a health insurance plan, it’s still far more complicated than it should be.

To pick a plan you can be confident is the (likely) best plan, I strongly recommend plotting up your actual OOP over a wide range of expenses for a variety of plans.

Then you can pick the plan that is cheapest for your expected level of dental expenses.

Wonderful insights covered on dental insurance plan.

Thanks Randy!