For quiteawhilenow I’ve been interested in figuring out how subsidies are calculated for Affordable Care Act (ACA) health insurance (probably better known as Obamacare, but I prefer ACA because it’s shorter to say and write).

Why? Because health insurance, and all the stress of how to get it when you don’t have access to employer-provided insurance, is a big topic in the Financial Independence (FI) community.

Unfortunately I ran out of time to do much of any stress testing analysis, but I did run it for a couple scenarios and compared the results to the Traditional method for those scenarios – and the results are very promising!

It’s been another week of lots of work and coding and testing. But, still no results for the stress testing analysis unfortunately. I did come up with a pretty large breakthrough though (I think, TBC once I have results), for handling the main problem I was facing last week.

But as I wrote that post, one question kept popping into my head: instead of striving for a $0 tax bill until age 72 (as is the default in the TPM method), could it be worth it to pull more from your pre-tax accounts (beyond the standard deduction) and thus pay a small amount of taxes earlier in your retirement to further reduce your pre-tax account balance and thus reduce RMDs and taxes after age 72 (soon 75)?

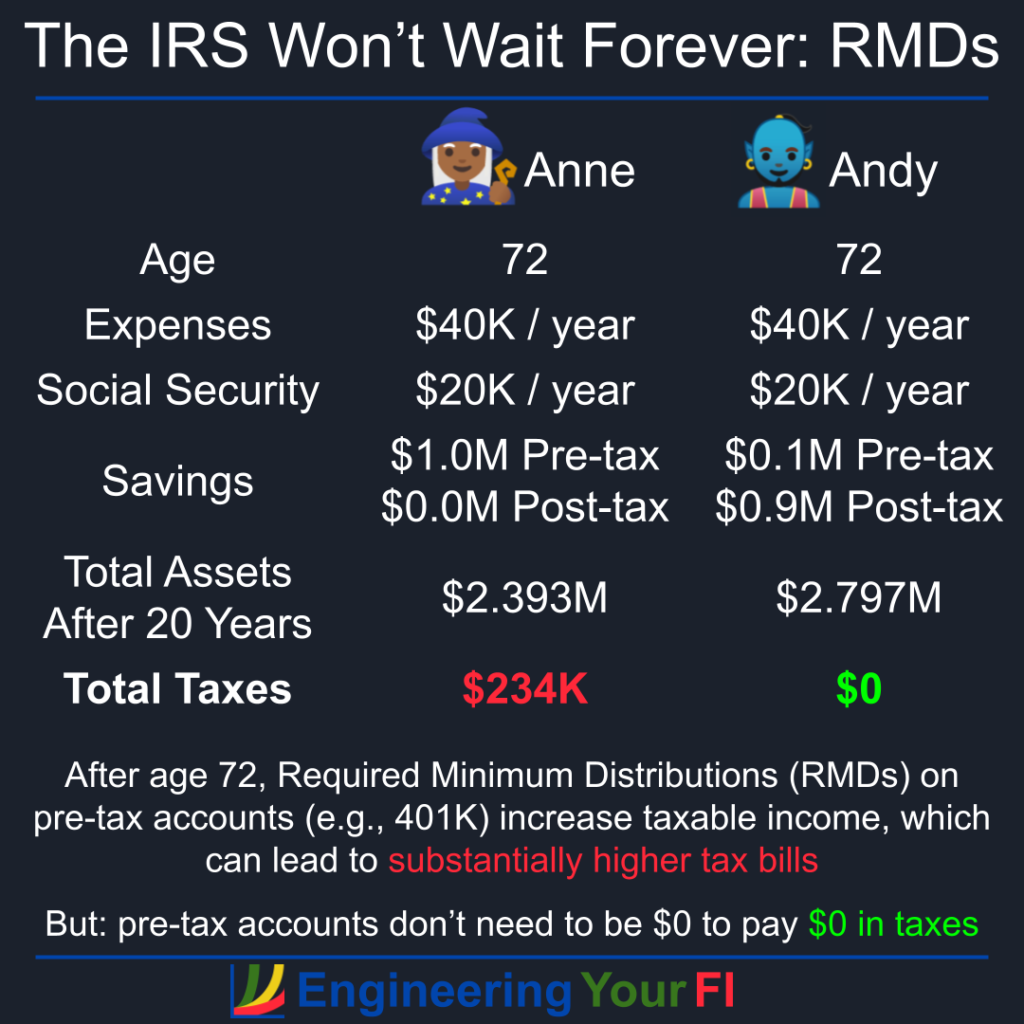

In this post, we’re going to show just how much better the TPM method is than the traditional withdrawal method for reducing RMDs and thus your tax bill. Especially if you’re an early retiree and can take advantage of decades of good tax planning.

If you’re focused on FIRE (Financial Independence and Retiring Early), it’s easy to sweep topics like Required Minimum Distributions (RMDs) under the rug. Those don’t start until age 72! That’s decades from now!

But an early retiree is in a unique position to take advantage of decades of tax planning – which means we can hopefully minimize taxes over our ENTIRE LIFE, including the span when we’re forced to take RMDs.

But before we dive into how to minimize lifetime taxes that includes RMDs for an early retiree, we need a good understanding of what they are and how they work.