Last updated: October 28, 2023

Last week at FinCon (review post coming soon!) I had the privilege to meet Emily Roberts, who hosts the Personal Finance for PhDs podcast and has helped many PhD students with personal finance since she graduated with her PhD in biomedical engineering in 2014.

As far as I know, she is the first fellow PhD in engineering I’ve ever met at FinCon, which was really nice – there aren’t too many of us interested enough in personal finance to go to a conference about it!

One question we discussed was whether grad students should invest any savings they can scrape together in a Traditional IRA (which is fully deductible, equivalent to 401(k) “pre-tax” dollars) or a Roth IRA (which you contribute to after paying taxes, but grows tax-free after that).

What makes this question interesting is that grad students are typically in a pretty low marginal tax bracket due to a pretty low (or zero) income.

My initial gut reaction was that it would still be better for those students to put their savings in a Traditional IRA, despite the low marginal tax bracket. However, I wasn’t sure, so I decided to do some fun personal finance analysis!

Example Scenario And Assumptions

For the analysis below, I came up with the following scenario:

- A single 20 year old student saves up $1K to invest (I know most graduate students are older than 20, but it’s a nice even number, and this same analysis applies to undergraduates who have a job)

- They invest this $1K into a Traditional IRA, or they invest $880 ($1K minus a 12% tax) into a Roth IRA

- They pay 12% in taxes because I assume their top marginal tax bracket is 12%. In other words, their total standard income is greater than the standard deduction of $13,850 plus the top of the 10% bracket $11,000, or $24,850 (which I think is reasonable in 2023, even if it was definitely not back when I was in graduate school!)

I’m not going to consider the scenario where a student is in the 0% tax bracket (i.e. all standard income is less than the standard deduction), because if that’s the case there’s zero benefit to contributing to a Traditional IRA instead of a Roth.

We’re going to look at the total “cash-out” balance of each option (Traditional vs Roth IRA) for a wide range of years – from age 21 to 90.

This will include accounting for taking a 10% penalty plus taxes for any Traditional IRA withdrawals before age 59.5, and a 10% penalty plus taxes for any growth of the Roth IRA before age 59.5.

Any original contributions to a Roth can be withdrawn tax and penalty free (and any withdrawals you make on a platform like Vanguard or Fidelity are essentially counted as taking out the original contribution first when filing your taxes).

In the analysis below we’re going to consider a range of “withdrawal tax rates” – the top marginal tax bracket (which we’ll assume applies to the entire withdrawal) based on the income of the student later in life.

These top marginal tax bracket limits will be different if the student marries in a subsequent year and files jointly, but the tax rates for each bracket remain the same (10%, 12%, 22%, 24%, 32%, 35% and 37%), so the results below apply for students that marry later on.

To simplify the results and keep this post/analysis from being too long, I’m going to consider just three withdrawal tax rates: 0%, 12%, and 24%. I believe we can gather the necessary conclusions from just those three rates, but of course you can plug in your own rates in the python tool I’ve built and link to below.

Other assumptions I’m making:

- All input and output dollar amounts are in present-day dollars. So if you find yourself thinking “well what about inflation?”, then remember that we’re keeping everything in today’s dollars.

- I’m using an after-inflation (real) annual return on investment (ROI) of 5%, which I get by assuming the student invests around 70% in equities (which historically return around 7%) and around 30% in bonds (at a conservative real ROI of 1%).

- The age at which you can withdraw from retirement accounts will remain 59.5 in the future (which could easily get pushed out in the future as people live longer, but there’s no way to know when or if that will happen).

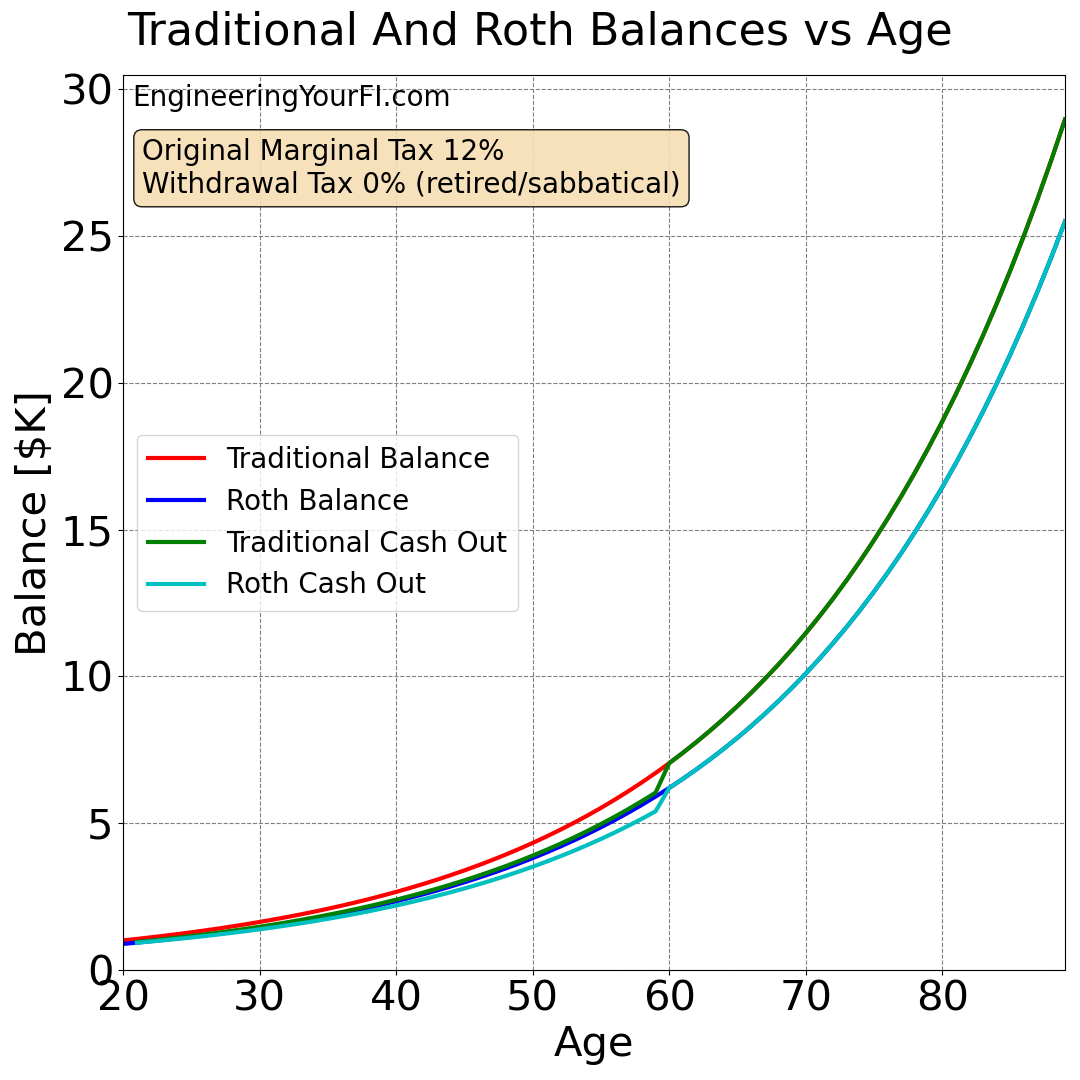

Withdrawal Rate of 0%

The first withdrawal tax rate we’ll consider is 0%. This is quite possible to achieve if you’re retired (early or not) or are taking a sabbatical that encompasses an entire calendar year. In essence, your standard income (which doesn’t include long term capital gains) does not exceed your standard deduction.

Below is a plot showing the balance of the Traditional IRA and Roth IRA accounts for each year from age 20 to 90, as well as the total “cash-out” amount you could get from each account:

You can see how the Traditional IRA balance and cash-out amount remain above the Roth balance and cash-out amount for all years. This makes sense, because the withdrawal tax rate (0%) is lower than the initial tax rate (12%).

You can also see the step up of the cash-out values to equal the exact account values at age 60 (well actually 59.5, but I’m using whole integer ages here), which early withdrawal penalties drop away.

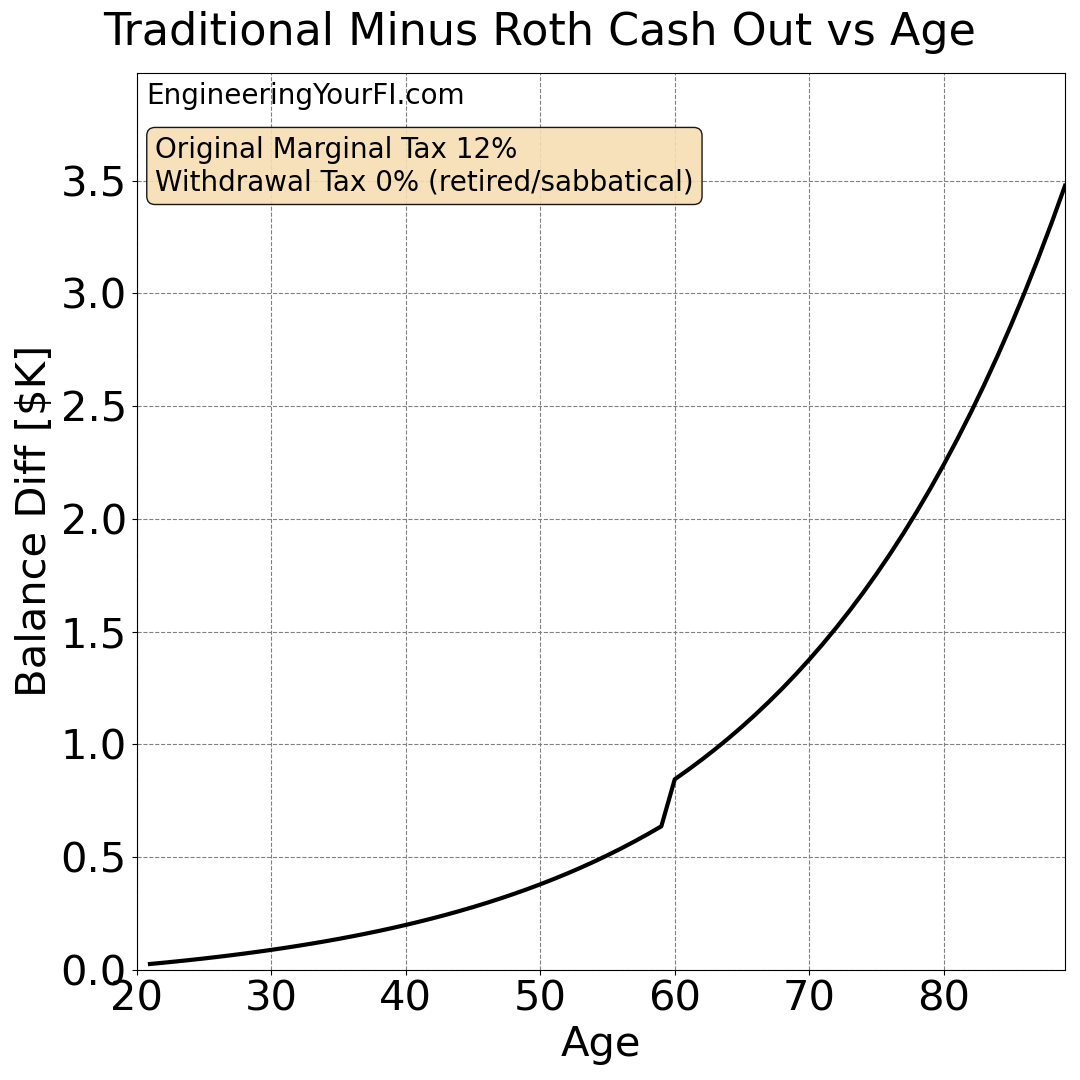

Let’s plot the difference of the Traditional and Roth cash-out balances as well:

You can see how the difference in the cash-out value of both accounts is pretty minor until you get into your 50’s and 60’s, but it goes up quickly from there. In your 60’s, you’ll have around $1K or more by investing in a Traditional IRA in grad school instead of a Roth IRA. Nice!

Also interesting is how the difference jumps at age 60 when the penalties no longer apply – another reason to wait until 60 if you can (or use a Roth ladder as described below).

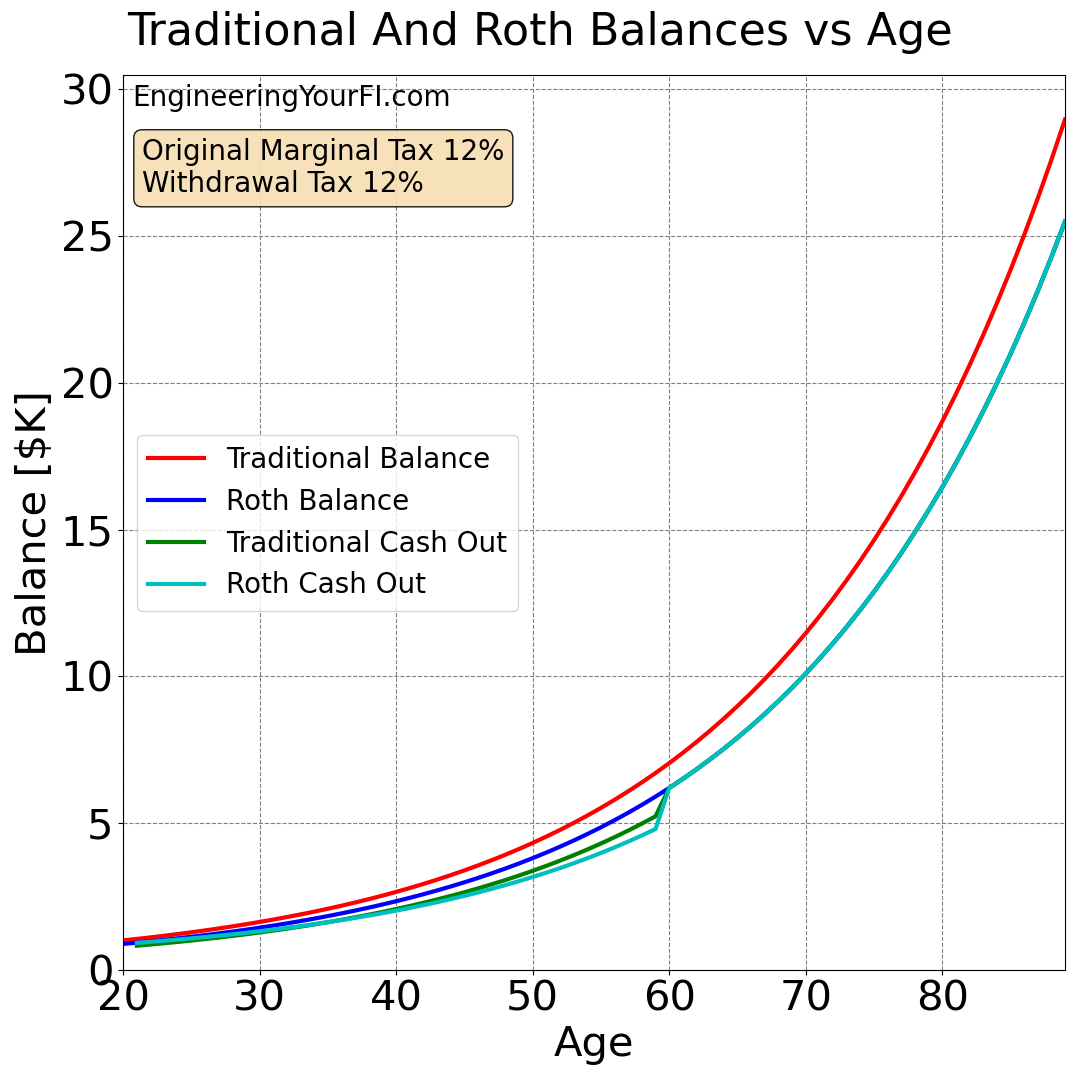

Withdrawal Rate of 12%

Now let’s consider a withdrawal tax rate of 12%. In other words, your top marginal tax bracket is 12%, and the entire withdrawal falls within that bracket.

For those that use their degree to obtain a high income, this might only be possible after retirement or via a sabbatical that’s long enough to get your standard income within the 12% marginal tax bracket.

Below is a plot showing the balance of the Traditional IRA and Roth IRA accounts for each year from age 20 to 90, as well as the total “cash-out” amount you could get from each account:

You can see that starting at age 60 (when the early penalties drop off), the cash-out balance of both accounts is identical. Which is logical – you’re paying the same tax rate when depositing and when withdrawing.

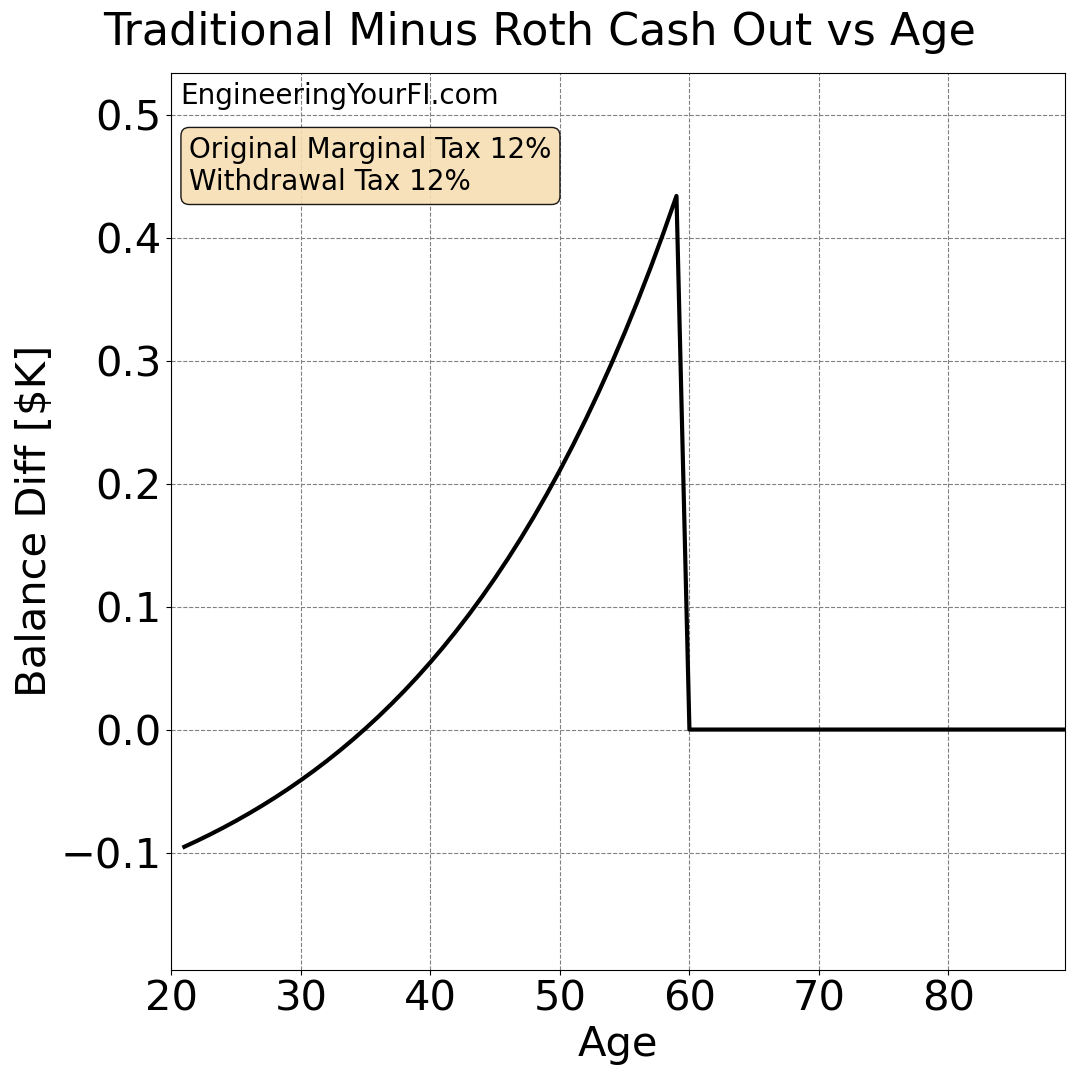

Before age 60 it’s a bit harder to see how the Traditional IRA cash-out value compares to the Roth IRA cash-out, so let’s plot the difference:

Interestingly the Traditional IRA cash-out value lags the Roth IRA cash-out before age 35, and then exceeds it from age 35 to age 60 (really 59.5). Why?

Before age 35, the growth of the Traditional IRA and the Roth IRA are small enough that the 10% penalty + 12% taxes on the entire Traditional balance is worse than the 10% penalty + 12% taxes on the Roth growth.

After age 35, the additional growth of the Traditional over the Roth (since it starts with a higher balance) results in a Traditional cash-out balance that exceeds the Roth cash-out balance. In other words, the original contribution to the Roth is now a much lower percentage of the total balance, so a majority of the Roth balance you’ll have to pay penalties and taxes on, AND it starts with a lower initial balance than the Traditional account (due to paying taxes up front).

SO, that means that if you think you’ll want to withdraw from your Roth account before age 59.5, but after age 35, and that you’ll be in the same tax bracket as you were in school, it can still be beneficial to choose the Traditional over the Roth.

Again this assumes a total liquidation (remember that you can withdraw the original contribution of the Roth penalty and tax free always), and that you’re not taking advantage of a Roth ladder to pull funds from the Traditional account penalty-free (see Roth Ladder section below).

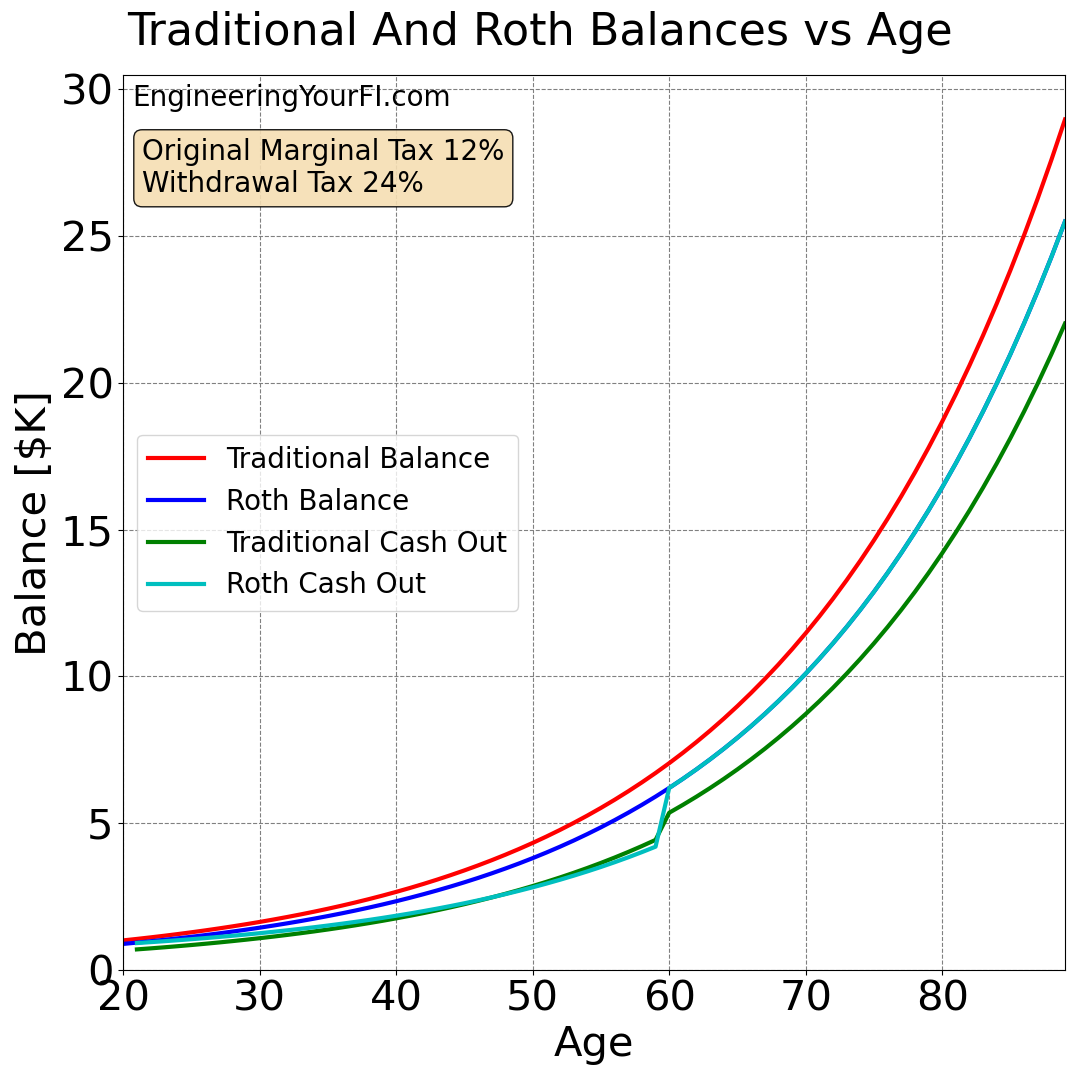

Withdrawal Rate of 24%

Now let’s consider a withdrawal tax rate of 24%. In other words, your top marginal tax bracket is 24%, and the entire withdrawal falls within that bracket.

For those that use their degree to obtain a really high income, this might only be possible after retirement or via a sabbatical that’s long enough to get your standard income within the 24% marginal tax bracket.

If your income prior to retirement or in retirement is high enough to exceed the 24% top marginal tax bracket ($182,100 for single, $364,200 for married filing jointly in 2023), I suspect you probably have more than enough money already to cover your expenses and this analysis is less relevant for you.

So I’m not going to consider a higher withdrawal tax rate than that. And I think the overall trend / conclusion is identifiable without going to higher rates anyway.

Below is a plot showing the balance of the Traditional IRA and Roth IRA accounts for each year from age 20 to 90, as well as the total “cash-out” amount you could get from each account:

You can see that starting at age 60 (when the early penalties drop off), the cash-out balance of the Roth significantly exceeds the Traditional. Which is logical – your top marginal tax rate is double the rate you paid back in school when you contributed to the Roth.

So if you are very confident that in your traditional retirement years (three to four decades after you graduate) you will be in a higher tax bracket than you were in grad school (despite not working), then it definitely makes sense to go with a Roth when you’re in school.

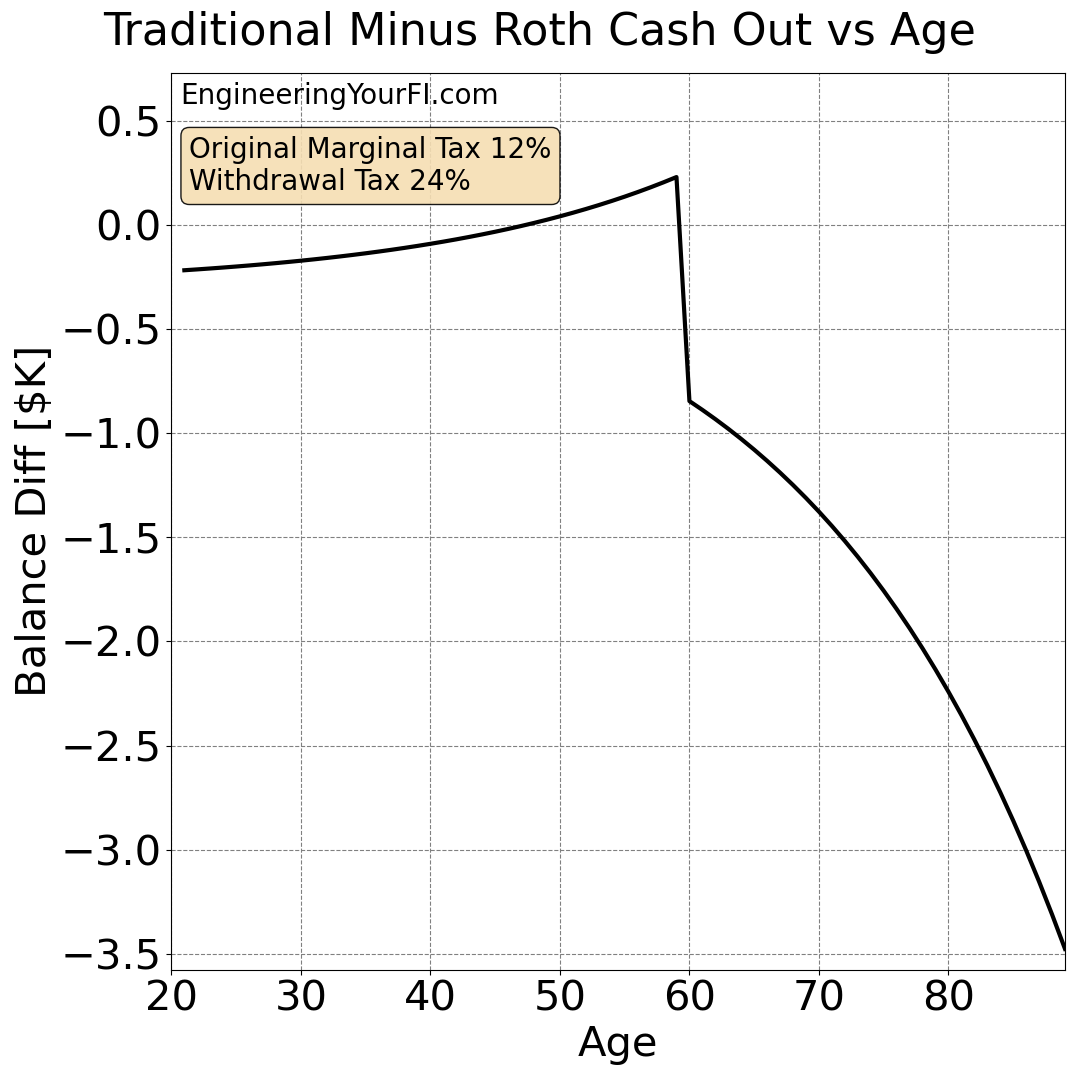

But as in the previous section, before age 60 it’s a bit harder to see how the Traditional IRA cash-out value compares to the Roth IRA cash-out, so let’s plot the difference:

Again you can clearly see how much better the Roth is after age 60 in this scenario.

What’s really interesting though is that there’s still a period of time when the cash-out value of the Traditional is better than the Roth, from about age 47 to 59. For the same reason I describe in the previous section: the additional growth of the higher initial Traditional balance and the Roth account consistently primarily of growth (which will have penalties and taxes if withdrawn) instead of original contribution. But it’s a pretty minor effect overall, and a relatively narrow span of time.

Uniform Withdrawal Amount (vs full cash-out)

All the comparisons above are in terms of “cash-out” value – but is that the best metric?

The Mad Fientist has a great article about how to access retirement funds early, where he considers a number of options such as the Roth conversion ladder, the 72(t) Substantially Equal Periodic Payments (SEPP), and just taking the 10% penalty.

He does assume a lower tax rate in retirement (15%) than while working (25%) though, so many of his results are not applicable in this analysis.

However, he does show an interesting metric at the end of the post that I wanted to test here: if you pull out a constant amount of money from each account per year, does one account last longer than the other?

This is different from the full “cash-out” value of each account, and I think it also aligns better with reality: people don’t typically just liquidate an entire account – they usually withdraw the amount they need to cover expenses each year.

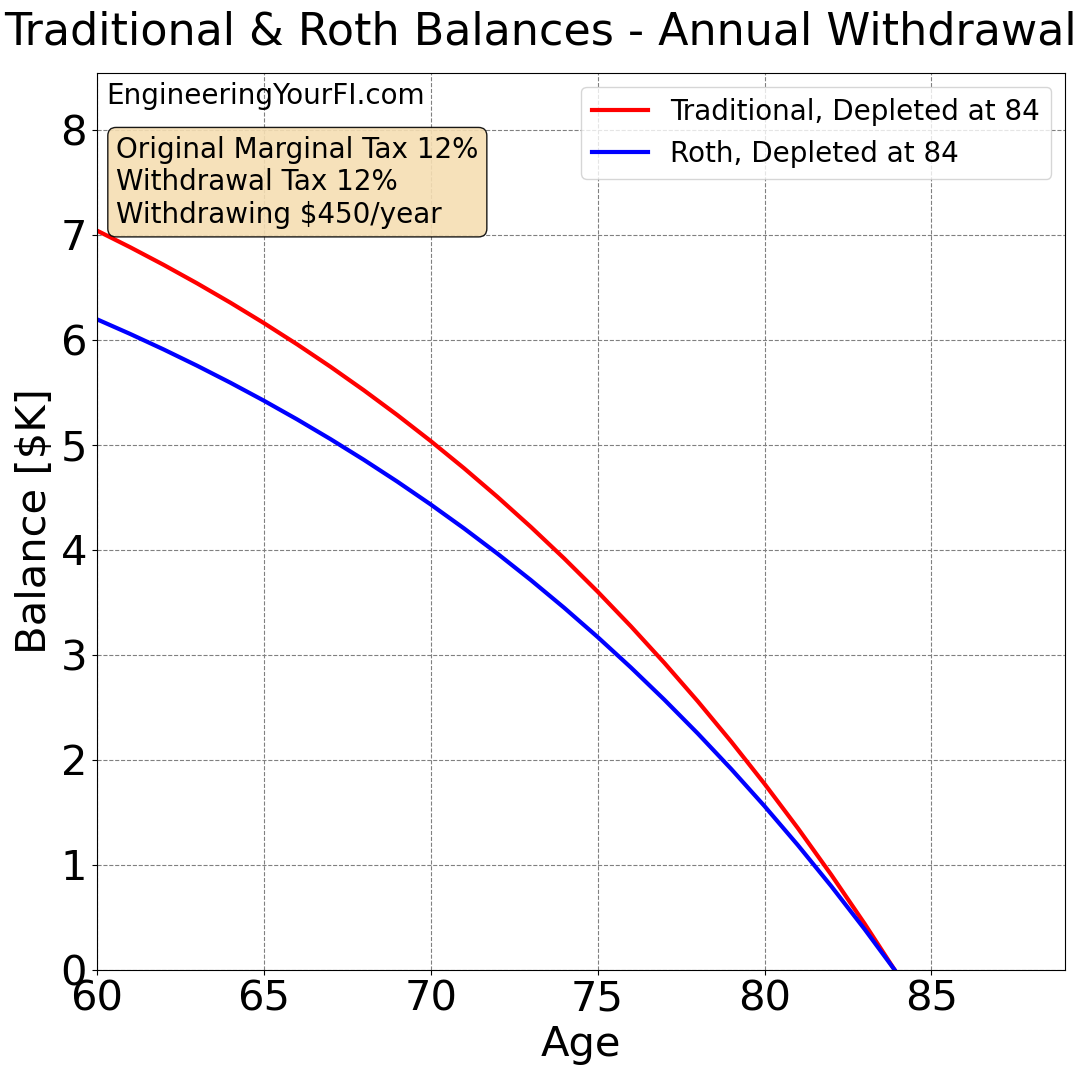

So let’s assume you have a withdrawal tax rate of 12% (so the Roth and Traditional exactly equal each other after age 60), and you want $500 (again in today’s dollars) from each account every year from age 60 onwards.

At a tax rate of 12%, that means you’ll be withdrawing $500 / (1 – 0.12) = $568.18 from the Traditional account, and $500 from the Roth.

In that situation, both types of accounts run out of funds at the same time: age 80.

Going with $450 instead of $500, both accounts run out at age 84.

Going with $400, neither of the accounts runs out of money before age 90.

Below is a plot of the account balances with the $450 scenario:

So this alternative metric leads to the same result as we saw in the previous section that considered a 12% withdrawal tax rate: the Traditional and Roth options are equivalent after age 59.5

And it makes sense: instead of paying that 12% tax on the Traditional in one go, you’re just spreading it over time.

Roth Conversion Ladder

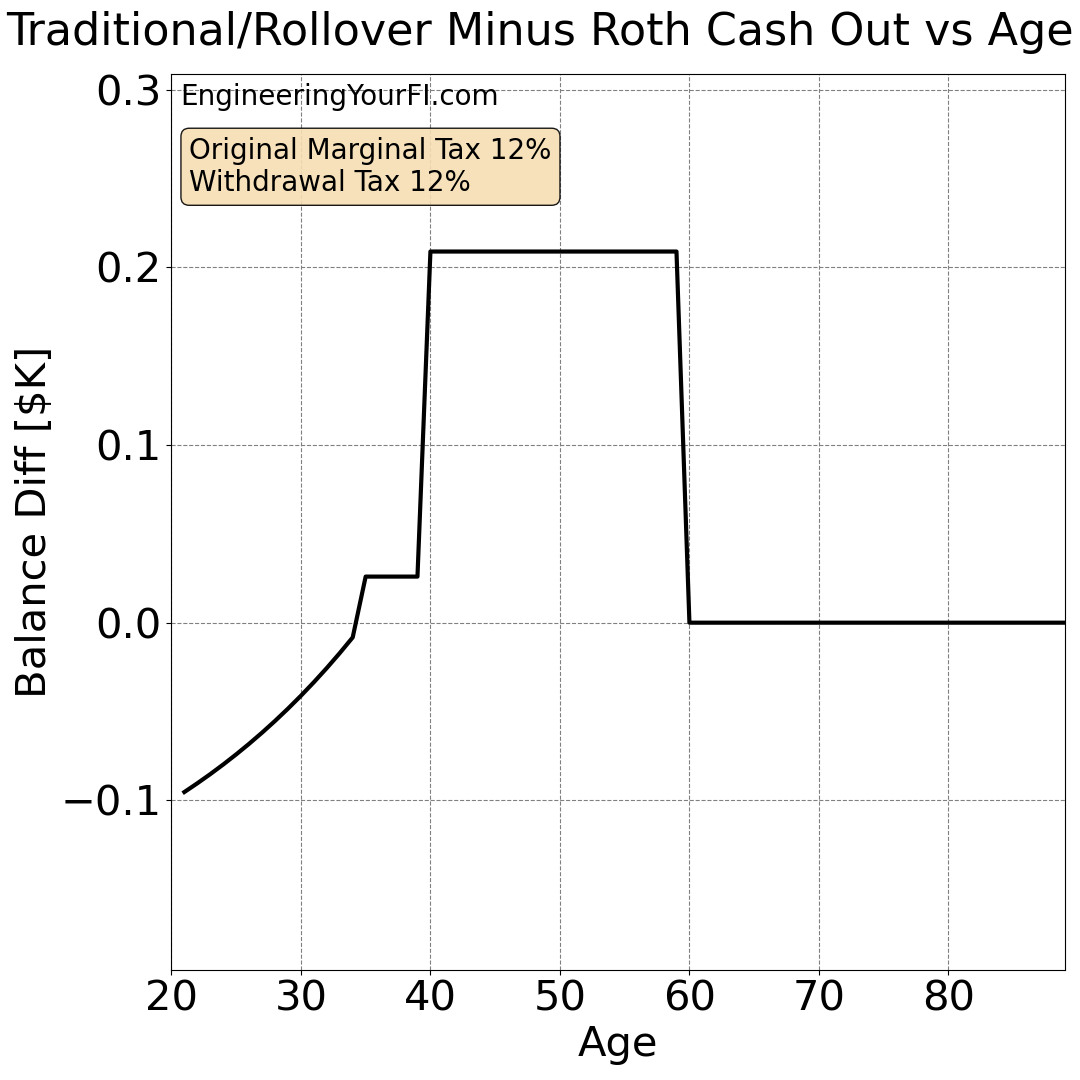

Now let’s consider the final scenario: doing a Roth Conversion Ladder.

Let’s assume you work until age 35 and FIRE at that point. You then immediately start a Roth ladder, rolling over at a 12% tax rate. Though I think it’s very doable to have a 0% tax rate in early retirement). But a 12% rate keeps things “fair” in terms of input vs output and thus we can see any specific benefits of the Roth ladder itself.

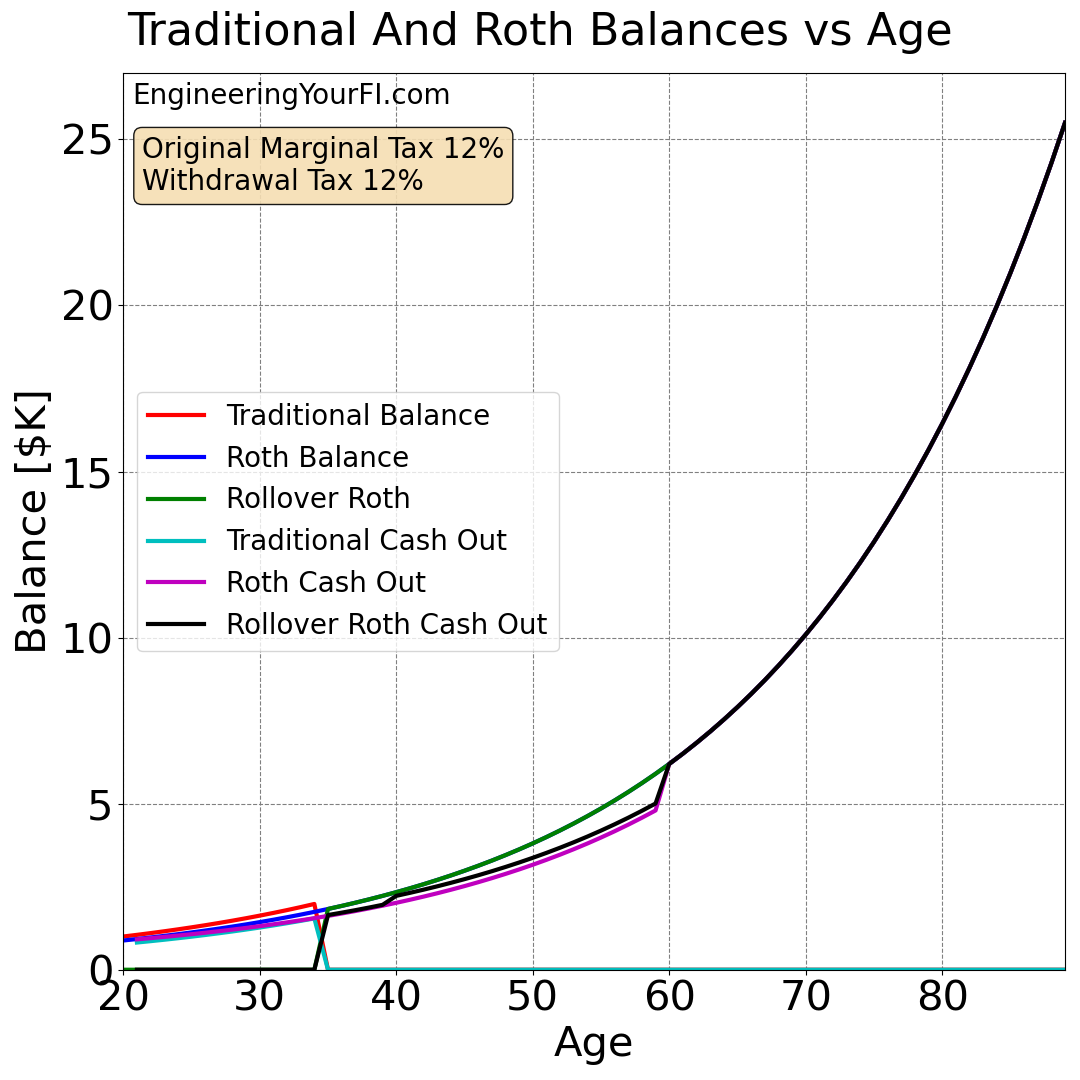

Thus in scenario #1 you initially invest in a Traditional IRA, let that grow until FIREing at age 35 (which is very doable if you save at least 50% of your income), and then you roll over the entire balance of the Traditional account (from just this single $1K contribution) to a Roth account at age 35.

In scenario #2 you initially invest in a Roth IRA, as described above.

Let’s calculate the cash-out value of each scenario:

You can see how the Traditional account (and thus cash-out value) goes to $0 at age 35 and the Rollover Roth account comes online at the same age, when you do the rollover.

As usually, everything is identical starting at age 60. But let’s plot the difference in the cash out values to see better what’s going on before age 60 (where I show the Traditional – Roth difference before age 35 and the Rollover Roth – Roth difference after starting at age 35):

Very interesting! Until age 35, you’re better off investing in a Roth initially, but after you hit age 35 and do the rollover, you’re actually better off doing Traditional initially and then rolling over at 35.

Why are the lines flat from age 35 to 39, and 40 to 59? And why is there a big jump from age 39 to 40?

The flat lines represent the higher “initial contribution” balance of the Rollover Roth vs the Roth – which can be taken out tax free. The higher “initial contribution” balance is because the Traditional account balance, even after paying 12% in taxes, is obviously higher than the $880 the student put into the Roth back in grad school.

So from age 35 to 39, you can pull that higher initial contribution balance of the Rollover Roth with just a 10% penalty, vs the normal Roth where you’ll be able to pull the much smaller original contribution with no penalties or taxes but most of the balance will be growth of the account that is both penalized and taxed if withdrawn.

Then at age 40, when the funds in the Rollover account are at least 5 years old and you can pull that higher rollover contribution without any penalties, the difference of the two scenarios is even greater – hence the big jump up in the plot.

Of course this effect is still pretty minor – just a couple hundred dollars in this scenario. Overall the primary factor in your decision should still be input vs output tax rates you expect to have.

Conclusions

The primary conclusion of all this analysis is that if you expect to have a lower top marginal tax rate when using the money later in life than you have in grad school, you should contribute to a Traditional IRA. And if you expect to have a higher top marginal tax rate later in life, it’s better to contribute to a Roth. And if you expect it to be the same rate, it’s roughly a wash.

I would argue that it’s very possible and desirable to have a 0% tax rate in retirement (early or not) or when taking a sabbatical, and thus if you have a tax rate above 0%, you should contribute to a Traditional IRA instead of a Roth IRA.

But if you are really convinced you won’t be able to stay in a 0% top marginal tax bracket, then going with a Roth in grad school is likely the better option.

A few other benefits for picking the Roth:

- There are no Required Minimum Distributions for Roth accounts, so you may face lower taxes after age 72

- A Roth IRA is the best option to leave to inheritors, if you believe you’re unlikely to ever spend that money

- If you’ve never opened a Roth before, it’s good to do that ASAP, because of the 5 year rule (you must have opened a Roth account anywhere at least 5 years before to withdraw earnings tax-free, so you need to have opened an account by age 54.5 at the latest to withdraw those earnings tax-free at age 59.5)

A benefit of picking the Traditional over the Roth though:

- If you retire early and need to “manufacture” income to ensure you have enough income to qualify for ACA subsidies, a rollover from Traditional to Roth can generate that income for you

If you do pick the Traditional IRA and find that you need the funds earlier than 59.5 (e.g., retiring early), I strongly recommend using a Roth Conversion Ladder to get those funds without penalty.

Code

I’ve placed the analysis code I used to generate the above plots in the EYFI github repo, which you’re welcome to download and run yourself if you’d like to plug in your own values or just play around with different inputs.

When I get more time, I will also place an embedded Python interpreter here as well, so you can run the analysis directly from this page.