Last updated: June 23, 2023

Note: The original version of this post was different in a number of ways, but after an excellent conversation in the comments below with the famous Big ERN (well, famous in FI circles, which means he’s famous to me), in which he did a great job explaining the motivation for using low discount rates when determining the best social security start age (better than I’ve seen anywhere else), I decided to make a number of changes. Those changes included reducing the scope of this post, and setting some remaining questions as future work.

As I say at the top of this post, this is the most requested topic I’ve received, so I want to do everything I can to get it right! And this is a great lesson in truth-seeking as well: always be willing to completely change your views/opinions if the evidence supports a different conclusion. Especially if you have a great reviewer such as Big ERN (who I suppose is acting like one of the many journal paper reviewers I’ve had many times and learned many important things from).

- Assumptions

- Default After-Inflation (Real) Annual Return On Investment (ROI)

- Default Inflation Adjusted Average Income

- Results – Using Default Values

- The Best Age To Start Social Security – Using Default ROI

- Results – Using Higher ROI

- The Best Age To Start Social Security – Using Higher ROI

- Results – Range of ROIs

- Results with Different Income Levels

- Future Work

- Conclusions

- Code

- Summer Schedule and Travel

When to start taking social security benefits is by far the most requested topic I’ve received.

But I couldn’t really tackle that question until I had a social security income model in place. Which I now have!

So let’s take a look.

Assumptions

As usual, we have a number of assumptions to address before diving into results.

1. All Values In Present-Day Dollars

All input and output dollar amounts are in present-day dollars. So if you find yourself thinking “well what about inflation?”, then remember that we’re keeping everything in today’s dollars so that we don’t have to mentally account for higher prices in the future.

2. The Minimum 40 Credits Are Obtained

A minimum of “40 credits” are needed to be eligible for social security benefits – otherwise you get nothing. So we’ll assume we have those 40 credits.

3. Full Retirement Age is 67

For everyone born in 1960 or later, Full Retirement Age (FRA) for social security benefits is 67.

Here in 2023, that means if you’re 63 or younger, your FRA is 67.

For folks born before 1960, the FRA is only a bit earlier (no lower than age 66 if you’re born in the 1950’s).

So given how little the FRA changes for folks born in the 1950’s (someone born in 1953 turns 70 this year, which is the latest age you can start social security), and that everyone born after the 1950’s will have the same FRA, we’ll just use a FRA of 67 in all the analysis below.

I’m also pretty dang confident all the results below will not be significantly impacted by a slightly earlier FRA, but we can easily check that in the future if desired. You can also provide a different FRA value in the tool provided below, and see how the plots change.

4. You Turn 62 in 2023 or Later

I make this assumption for two reasons: 1) so we can use the bend points published for 2023 when computing the Primary Insurance Amount (PIA), and 2) so we don’t have to apply Cost of Living Adjustments (COLA) to the PIA.

Just like for the FRA value above, I strongly suspect that having an earlier birthdate and thus different bend points and COLA on the PIA will not significantly impact the results / conclusions below, but we can easily check that in the future if desired. You can also provide a different value in the tool provided below, and see how the plots change.

5. No Earned Income Starting At Age 62

This is another pretty powerful assumption, but I think it’s a vital one.

We need “apples to apples” comparisons of the total money you can expect to have from social security income with different retirement start ages.

But if you have earned income above certain thresholds before reaching your FRA, then your benefits are reduced until reaching FRA. And then when you do reach FRA, they “recalculate your benefit amount to give you credit for the months we reduced or withheld benefits due to your excess earnings.”

On top of that complication, an ADDITIONAL complication is the tax implications of having social security income on top of earned income, especially if you have earned income for only a portion of the time you have social security income. Bleh!

At some point in the future I may try to look at optimizing social security starting age when accounting for additional earned income, but for now we’re just going to assume you’re not getting any more paychecks starting at age 62.

6. You Either Save And Invest All Your Social Security Income, Or It Offsets Withdrawals From Other Investments

To best assess the total lifetime potential of social security income, we’re going to assume that you either save and invest every penny of your social security income because your portfolio already supports your full retirement budget, or that the income offsets the same amount of withdrawals you’d normally make from your investments.

As a result, we’ll assume that your income provides a particular real (after-inflation) Return On Investment (ROI). The particular ROI to use is discussed in the next section.

If we didn’t make this assumption, and instead assumed that you have no invested assets and you will spend every penny of your social security income, then it’s pretty obvious the real ROI will be 0% (if you believe the social security income stream really does fully keep up with actual inflation). In that case, there is no way the money you receive from social security will earn any kind of interest.

Given that this site is focused on FI, I think it’s reasonable to assume most readers will meet this criteria.

Default After-Inflation (Real) Annual Return On Investment (ROI)

What the Experts Use

When I first wrote this post, I just assumed the best default real ROI (also referred to as a discount rate) to assume would be the long term after-inflation market equities ROI of 7%.

But that didn’t align with what I’d read from a number of other very solid sources.

For example, a recent working paper (considered “working” because it has not been peer-reviewed) by researchers at the Federal Reserve and Boston University titled “How Much Lifetime Social Security Benefits Are Americans Leaving On the Table?” was featured in Kiplinger’s April 2023 Retirement Report. How do I know this? My uncle sent the feature to me via snail mail (thanks buddy!). It was also featured on CNBC.

The paper states “As for the appropriate real discount rate, we take, as our baseline, a 0.5 percent real return. This is roughly the average real return on long-dated Treasury Inflation Protected Securities (TIPS) observed in recent years.”

The Open Social Security calculator uses a real discount rate of 1% by default, and it references an article by Mike Piper at ObliviousInvestor.com for why it has this rate as default.

Mike’s argument is that since this is considered “perfectly safe” income (ignoring the fact that the program is not sufficiently funded), you should use the best possible interest rate generally available for “safe” diversifying assets such as bonds as part of an asset allocation approach.

But that still didn’t convince me initially.

Finally, I had a great conversation in the comments with Karsten from EarlyRetirementNow.com, where he did a better job explaining this justification for a lower assumed ROI than I’ve seen anywhere else. He also has a relatively recent post about this very topic.

As a result, while I’m still not 100% convinced (see next section), I’m sufficiently convinced to use a 1% ROI as the default for the analysis in this post (even though the most recent TIPS long term real rate is 1.67%, but we’ll be more conservative here).

And if for some reason I become convinced it’s better to assume a higher ROI, the plots with different ROIs below will be very handy.

But I Still Don’t Fully Understand Exactly Why

I must admit I’m still not fully satisfied with just making this assumption that we should use the best possible interest rate generally available for “safe” assets.

Probably because I still don’t fully grasp from a first principles approach why this is true.

I’m a big believer in employing a first principles approach for all the analysis I do on this site, for a couple reasons: a) I really want to fully understand as much as I can, and b) so that I can determine if there are any details that might be different for a FI-focused audience.

For example, let’s say you have 70% equities and 30% bonds in a $1M retirement portfolio, and you withdraw a total of $40K from that portfolio each year. That means $28K from your equities, and $12K from your bonds.

But if you have $20K in annual social security income, you only need to withdraw $20K from your investments. Which means $14K from your equities and $6K from your bonds.

So if you’re withdrawing $14K less from your equities, why would you not assume a higher ROI than the best rate you can get for your bonds?

Why wouldn’t you assume a 0.7 * 7% + 0.3 * 1% = 5.2% ROI in that case?

I’m pretty sure it’s due to the *nature* of the social security income, because it’s considered “safe” income (none of the volatility associated with equities). But that hand-wavy answer is not really enough to satisfy my itch to understand. I still feel like I’m missing something.

In fact, once you have “safe” social security income flowing in, does that mean you should reduce your “safe” bond holdings accordingly, to better align with your short- vs long-term risk stance prior to social security starting? What does that mean for the assumed ROI when deciding your social security income start age?

So I plan to look at this more closely in a future post. But for now, I recommend just using the ROI value recommended by folks with a lot more financial analysis experience and education than I have. The odds of all the above experts being totally off is pretty dang low I suspect (but very importantly, you should always assume non-zero).

Default Inflation Adjusted Average Income

To pick a default Average Indexed Monthly Earnings (AIME), which is your inflation-adjusted average monthly earnings over your 35 highest earning years, I’ve gone with the most recent US national median salary of $1059/week * 52 weeks / 12 months = $4589 / month.

However, we will also vary this value in the analysis below, to consider lower and higher incomes.

Results – Using Default Values

Alright, let’s start building some juicy plots!

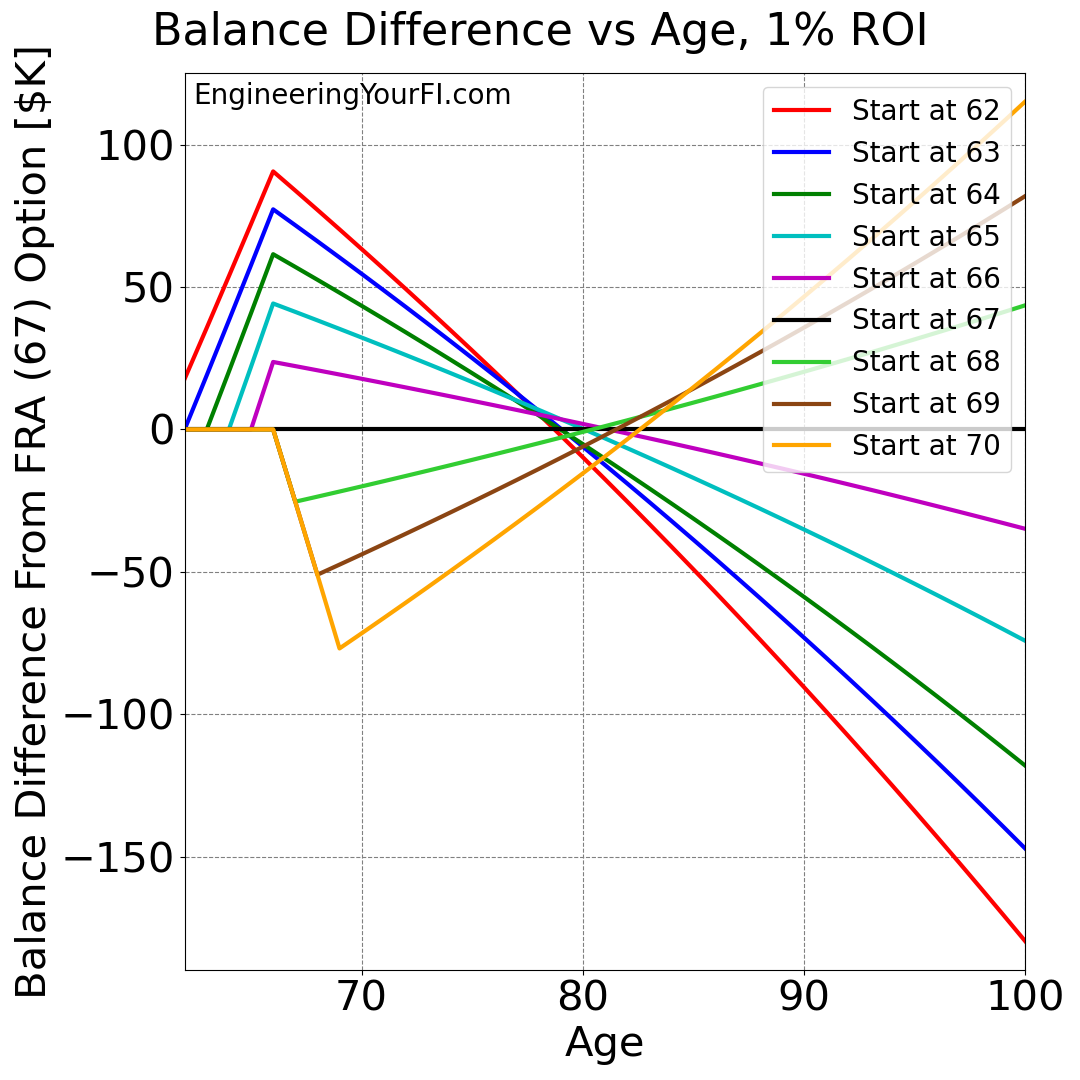

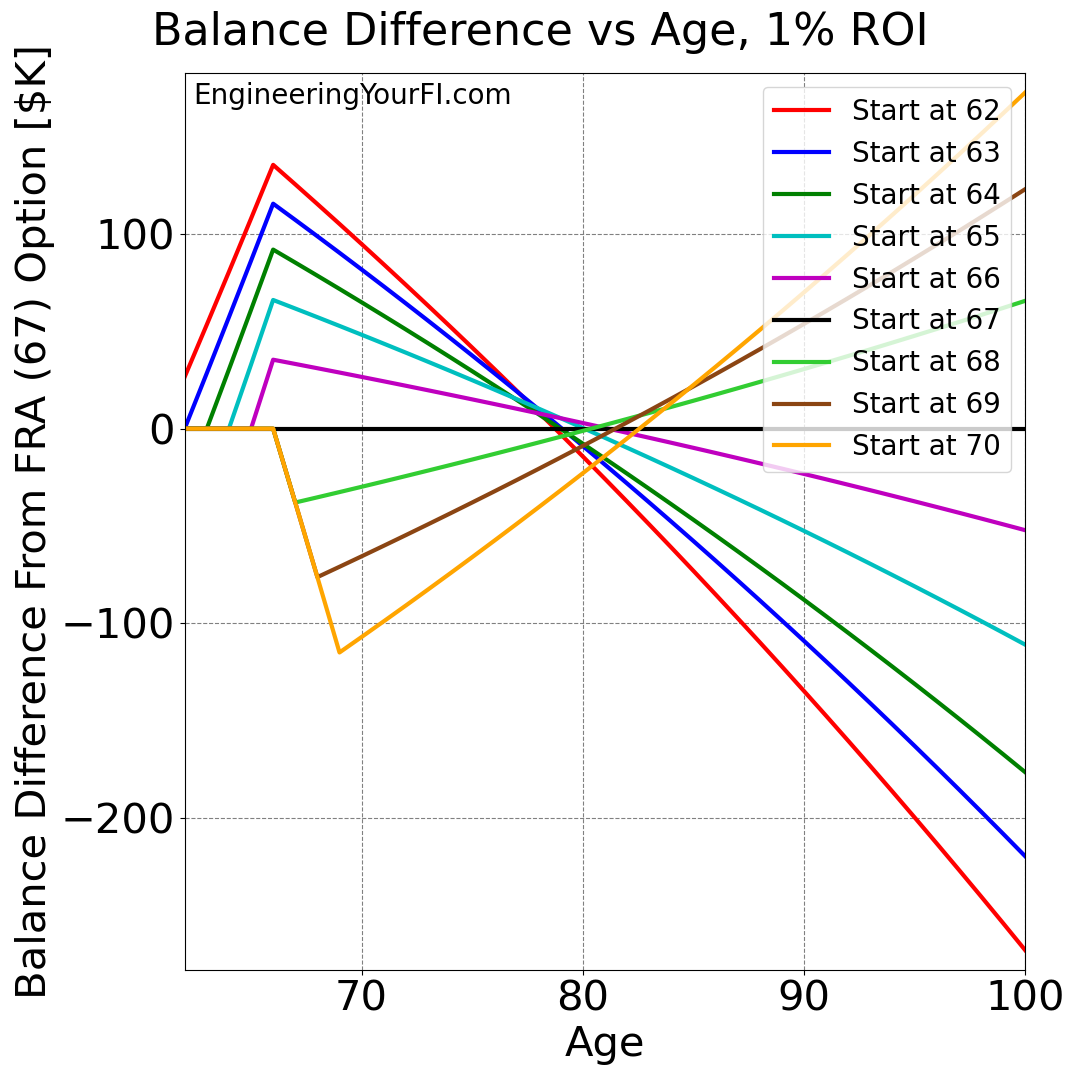

First let’s take a look at the total balance over time from social security income, using the default values of 1% for ROI and the US national median income of $4589 / month used to calculate the benefit.

Each plotted line represents a different starting age for taking social security, from age 62 (the earliest you can take social security) to age 70 (the latest you can take social security).

Unfortunately in this view it’s a bit difficult to see how each starting age option differs from the others. So instead we can plot how the balances differs from the “age 67” (FRA) line:

The balance difference plot shows the different “break-even” points between the different social security income starting ages, which are strongly clustered around age 80.

You can see how someone that starts social security at age 62 is up many tens of thousands of dollars versus someone that waits until age 70 for all of their 70’s. And then the opposite is true for all of their 80’s.

The Best Age To Start Social Security – Using Default ROI

So, if you assume a constant ROI of 1%, the best age to start social security essentially comes down to one main factor: how long you live.

If you think it’s extremely unlikely you’ll live beyond your mid-70’s, then you might be best off starting social security at age 62 – as early as possible. This might be the case if you have known health issues, bad lifestyle habits such as smoking, and/or you have a strong family history of dying relatively early.

If you think it’s very likely you’ll live until your late 80’s or longer, then you should put off taking social security as long as possible: age 70.

Using Actuarial Tables

What if you have no idea? And/or you’d prefer to use broad population-based actuarial table probabilities for how long you will live as calculated by the government?

(We’re getting into really fun ideas here, huh?)

A mistake I made in the first version of this post was using the average American life expectancy from birth, which is 76.4 in 2021.

Instead, it’s important that you use the remaining life expectancy that is published by the Social Security Administration (SSA) for your current age (different for men vs women).

That means if you’re a 62 year old male (the first age at which you’ll be facing a decision to start social security or not), your life expectancy is an additional 19.03 years, getting you to age 81. If you’re 62 and female, your life expectancy is an additional 22.04 years, getting you to age 84.

And guess what? Those ages are right in the region of all the “break-even” points seen above. That’s the nature of the social security program, which is designed to be “actuarially fair”:

“Social Security actuarial adjustment factors for early and delayed claiming are intended to be actuarially fair for an average beneficiary.”

And in fact, tools such as OpenSocialSecurity.com directly use these life expectancy / probability of death values when making recommendations on when to start social security.

But still, using these actuarial probabilities does not account for health factors only you can know about. So, I recommend treating these values as a good starting point for your own decision.

What the Experts Usually Recommend

Despite the fact that social security is supposed to be “actuarially fair”, and thus there should not be any statistically beneficial bias over the entire population towards taking social security earlier or later, many experts seem to recommend delaying starting social security to the latest possible age for most people.

For example, if we return to the working paper I mentioned above, they state in the abstract: “We find that virtually all American workers age 45 to 62 should wait beyond age 65 to collect. More than 90 percent should wait till age 70. Only 10.2 percent appear to do so.”

Waiting until 70 also seems to be the favored advice of most financial advisors.

Though be careful: some resources don’t factor in the time value of money, such as this fool.com article.

And those financial advisors might be working mostly with folks who don’t meet assumption #6 above (“You Either Save And Invest All Your Social Security Income, Or It Offsets Withdrawals From Other Investments”). In other words, they have little to no invested assets and will spend every penny of your social security income. In that case, holding off on taking social security is a good idea (purely from a financial perspective) if it forces a senior to work longer (and potentially reduce their overall spending) because they won’t have enough income to make ends meet otherwise. But hopefully if you’re reading this site, that won’t be a situation you face.

Sequence vs Longevity Risk

Now let’s add another layer of complexity to the decision process, just to make things more interesting (or nightmarishly more complicated, depending on how you feel about complex financial analysis).

Something Karsten and I discussed in comments below after I put out the first version of this post was the trade-off between reducing sequence of returns risk by starting social security income earlier (having more money/income earlier for any big downturns that happen soon after retirement), versus reducing longevity risk by starting social security income later (having more money later to ensure to you don’t run out of money later in life).

In other words, we also need to consider variable market returns when assessing what age to start social security.

In the future I would very much like to analyze this trade-off.

One question in particular I’d love to analyze: does it make sense to start social security earlier in your 60’s if the market is down heavily? (Especially if both equities and bonds are down?)

Also, if we’re talking about sequence risk vs longevity risk, that seems to imply that social security income will reduce equity investment withdrawals, which seems to imply a larger ROI than 1% should be used in our analysis. Even if it’s not fully 7%, but instead calculated based on the fraction of offset equity withdrawals. Not sure about this though.

A comment at the top of Karsten’s most recent post has me wondering if he’s also about to analyze this sequence vs longevity risk trade-off for the social security starting age decision. If so, I’m *very* curious to see what he comes up with.

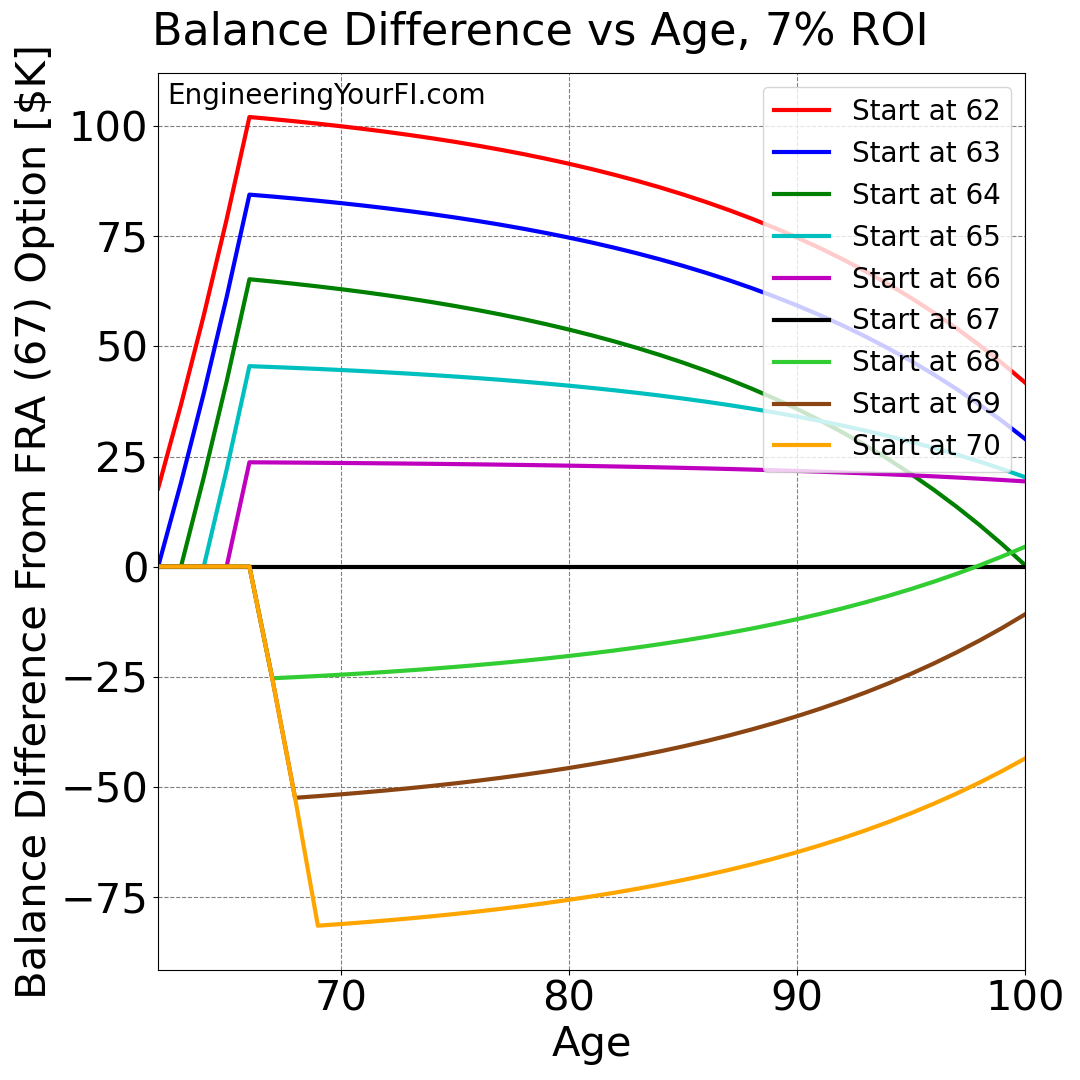

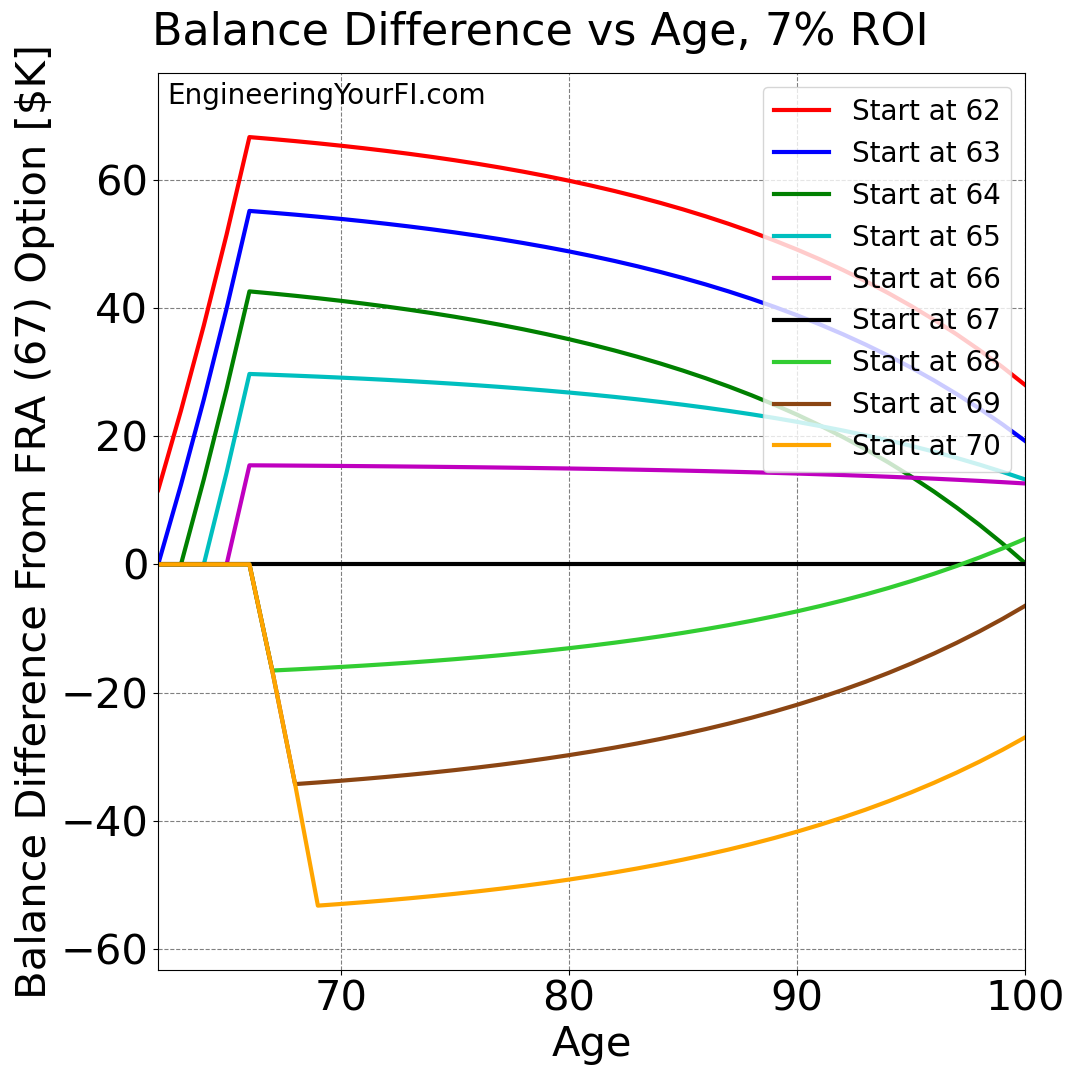

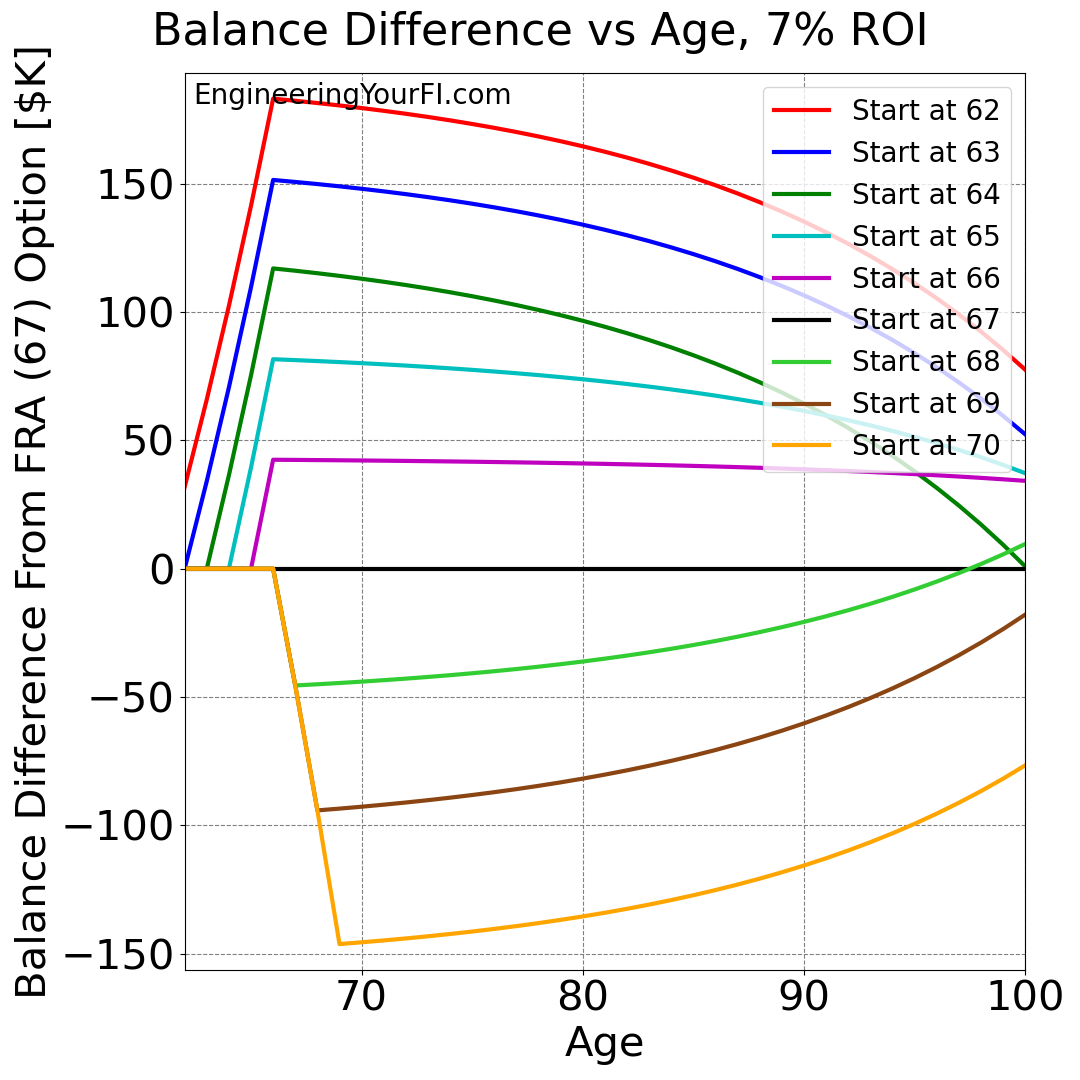

Results – Using Higher ROI

Despite shifting the default ROI used above to 1%, there does still seem to be a clear non-zero segment of folks that should still use the long term after-inflation market equities ROI of 7%.

The two conditions in which it still seems valid to use this 7% ROI are:

- You have a pension, business income, or some other kind of income that you are very confident will cover all of your expenses for the entirety (or nearly the entirety) of your retirement

- You have 100% of your investments in equities (which might be because of reason number one)

If you fall into one or both of these situations, then you can/will be investing any social security income entirely into equities (or it will offset withdrawals from your investments that are 100% equities), and thus you can assume an ROI of 7%.

So, what are the results of starting social security at different ages if we use this much higher ROI?

The Best Age To Start Social Security – Using Higher ROI

You can immediately see that if we assume a 7% ROI, taking social security as early as possible (age 62) ALWAYS WINS. And taking social security as late as possible (age 70) ALWAYS LOSES.

Sure enough, if you crank up the real discount rate on the Open Social Security calculator to 7%, then it consistently reports that you should start taking social security as soon as possible.

Even Mike Piper at ObliviousInvestor.com states that “The higher the rate of return you assume, the more advantageous it is to claim benefits early”. And that the primary exception to using the “expected return on the bond portion of their portfolio” would be “the household that has a 100%-stock allocation and wants to take on even more risk.”

In other words, Mike also seems to agree that if you place your social security income into equities and thus can assume a long term average ROI of 7%, then it makes sense to take social security earlier.

Big ERN also succinctly describes this scenario in the comments below: “The scenario where you could use the 7% IRR is where your benefits actually create a net investment in the stock market. Not a gross investment that still leaves you with a net withdrawal. And with the net investment, you like to maximize the final expected value, i.e., little or zero risk aversion. Then, sure, go ahead and discount SocSec by 7%.”

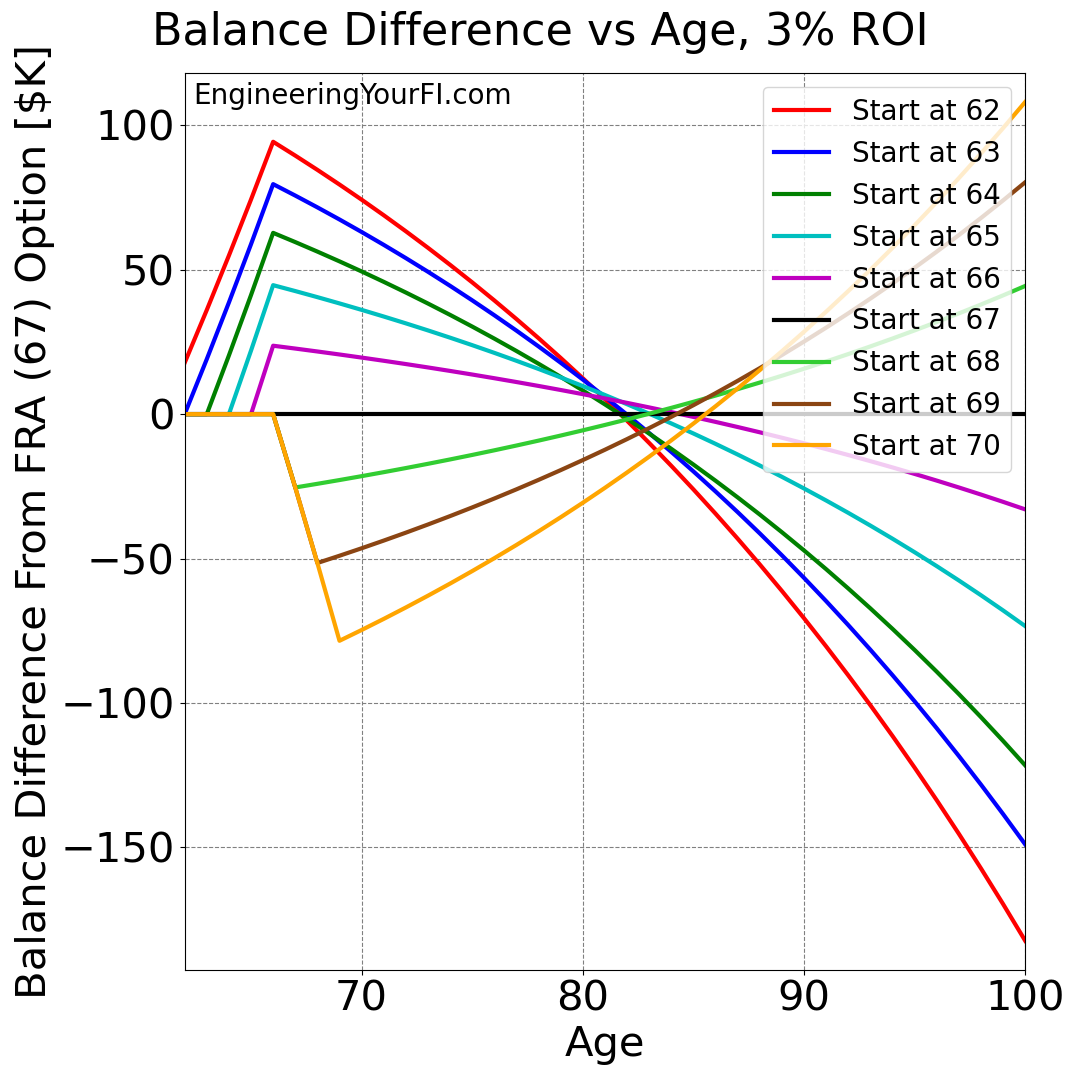

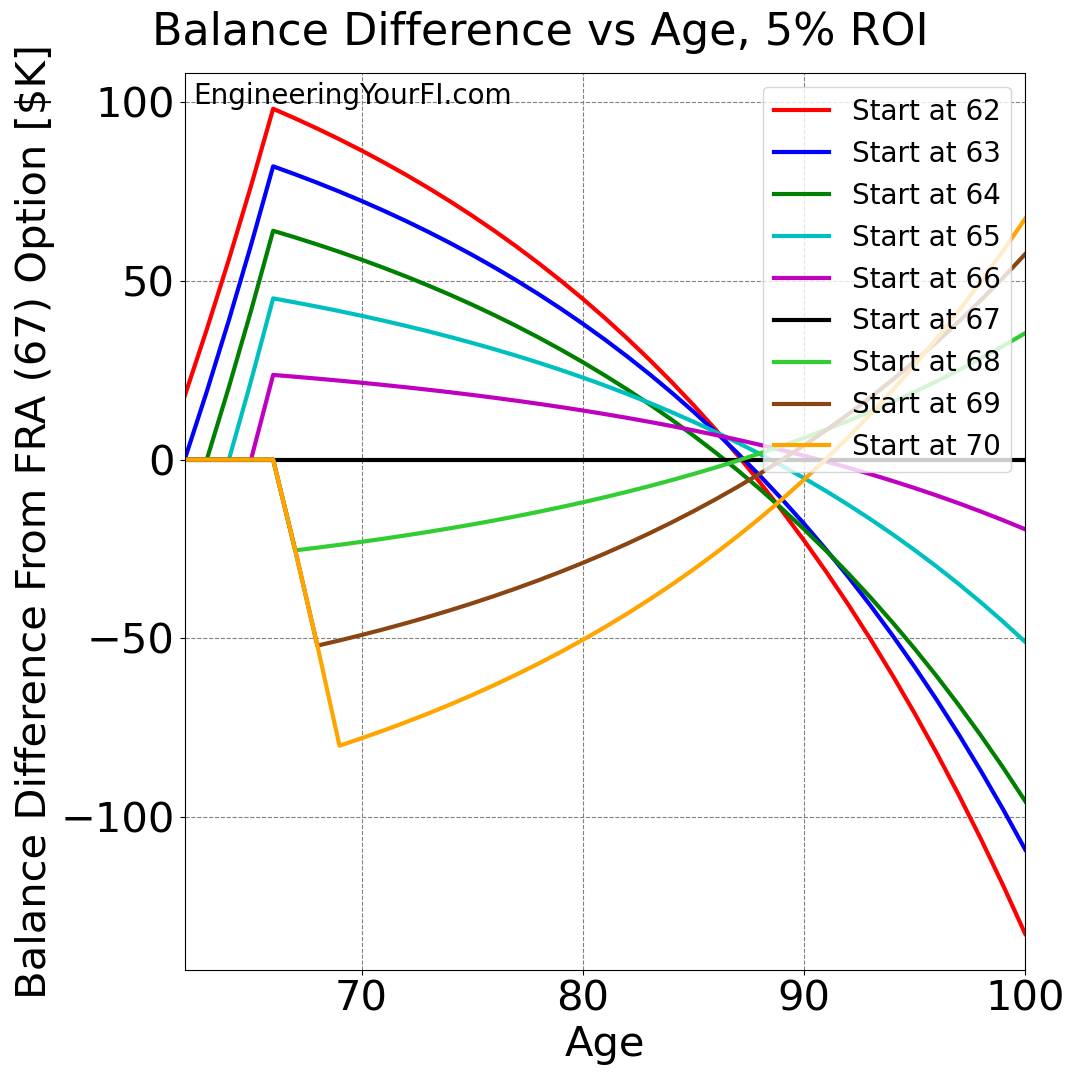

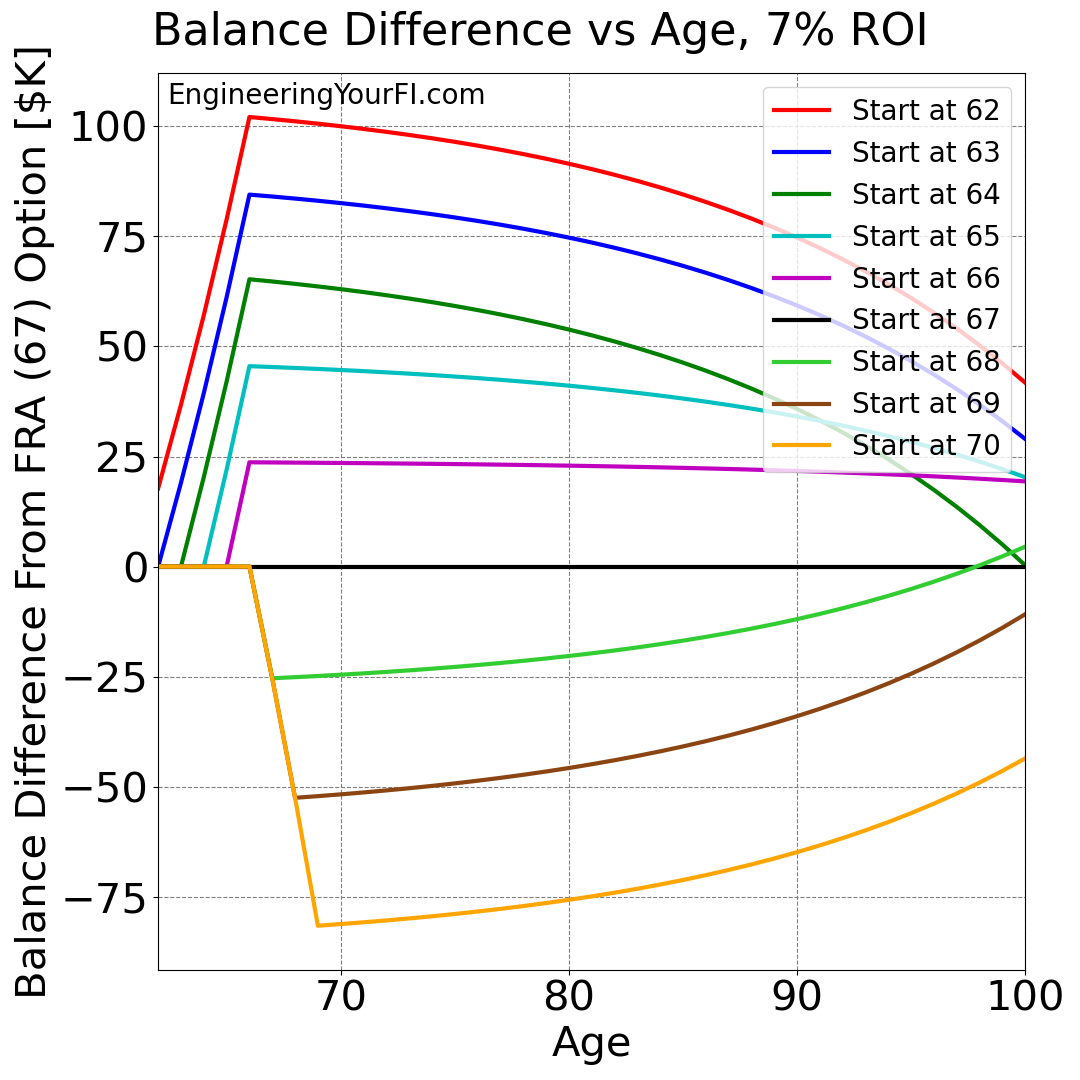

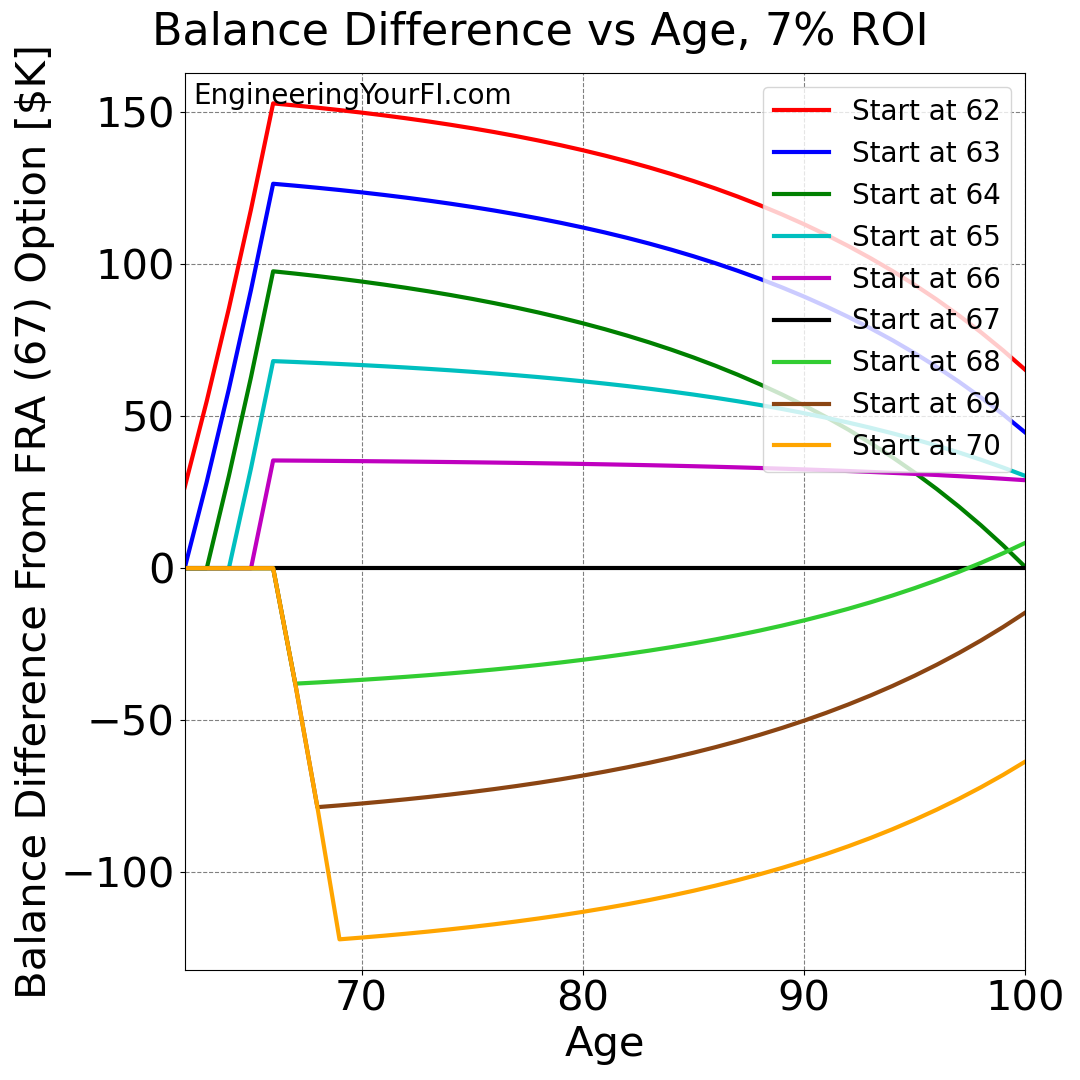

Results – Range of ROIs

Now what if in the end it makes more sense to use an ROI somewhere between 1% and 7%?

Let’s take a look at 3% and 5%:

You can see how the 3% and 5% ROI results lie between the 1% and 7% ROI results, as you’d expect. And as you’d expect given the 1% and 7% ROI conclusions above, the higher the ROI you assume, the more advantageous it is to take social security earlier. And the longer you have to live to see significant financial benefits if you wait to start social security later.

For example, if you assume an ROI of 5%, you can still do better in the end by waiting (vs 7% ROI where you never will), but you’ll need to live WELL into your 90’s to see any kind of appreciable benefit.

Results with Different Income Levels

So far we’ve only considered an AIME set equal to the most recent US national median salary of $1059/week * 52 weeks / 12 months = $4589 / month.

Let’s take a look at different AIME values now. Below are the results of using a 1% ROI and the following AIME values:

- $4,589 / 2 = $2,294.5

- $4,589

- $4,589 * 2 = $9,178

- $13,350 (the max AIME possible, given the max taxable annual income of $160,200 (2023)

AIME = $2,294.5

AIME = $4,589

AIME = $9,178

AIME = $13,350

You can see how for every income level, the plots look essentially the same – it’s just the y-axis scale that changes. But in terms of the relative performance of the different starting ages, everything is identical.

Now is this consistently relative performance just because of the 1% ROI? Nope. Below are the same plots if we use a 7% ROI.

AIME = $2,294.5

AIME = $4,589

AIME = $9,178

AIME = $13,350

Again, basically the same relative performance, with only the y-axis scale changing.

So overall the AIME seems to have no impact on the relative performance of the different starting ages, in terms of when the different break-even points occur for different starting ages (and thus what age you should decide to start social security).

In other words, your AIME doesn’t seem to be an important part of the decision on when to start taking social security – which really surprises me.

Future Work

As you’ve probably gathered by many of my comments above, I still see a ton more work that’s needed.

- Dive further into the question of what ROI is most appropriate to use, especially with regards to your asset allocation and how much equity withdrawals are offset by the social security income.

- Analyze the trade-off of mitigating sequence vs longevity risk described above. That might involve using historical market returns with a variety of asset allocations and starting social security ages. In particular I’m very curious to know the impact of starting social security earlier if the markets are down heavily at that time.

- Determine if having “safe” social security income flowing in means that you should reduce your “safe” bond holdings accordingly, to better align with your short- vs long-term risk stance prior to social security starting.

- Consider spousal and survivor benefits.

- Consider the impact of taxes on when to start social security, especially since up to 85% of your social security income can be taxable. Fortunately I have the social security taxation models fully implemented. This article on kiplinger.com indicates waiting to start social security could be quite beneficial in terms of taxes (see “Reason #3”).

- Consider how different social security income starting ages will impact of an equity glidepath (where you increase your equity exposure over time, as sequence risk drops).

- Consider how working into your 60’s can impact the best time to start social security, both in terms of any reduction in social security income and tax implications.

On a less important note, I know there are a lot of plots above, so eventually I may place collect those together as subplots to make it more manageable. But that might make the plots too hard to see as well – we’ll see.

Conclusions

When I first wrote this post, the answer for when to start social security in order to maximize its long term value seemed pretty dang clear: as soon as possible.

However, I’ve learned a LOT since then. And now unfortunately the answer is anything but clear. And I still have a lot of further analysis to do as well, as you can see from the Future Work section above.

From what I understand right now though, the main factors dictating when you should start social seem to be:

- Your health when you reach your 60’s, and how long you think you’ll live

- Your personal financial situation, including your asset allocation and income streams (especially if you’re still working in your 60’s), which impacts the ROI you should assume for social security income and your tax situation

- Whether you want to reduce the risk of running out of money in the near to medium term or the long term

- The state of the markets (maybe)

In the end, Mrs. EYFI and I may not decide when to start social security until we’re in our 60’s and we know the following things:

- Our health status, and whether we’re on track to likely live well past our 70’s

- Our financial status, including our asset allocation and income streams

- The state of the markets, especially if we’re at all concerned about sequence of returns risk (unlikely, but still)

- What (if any) changes to the social security program have happened between now and then

To analyze your own situation, you can log into ssa.gov, get the expected social security income amounts for different starting ages, and then put those into a spreadsheet. Then use your preferred ROI to propagate the balance over time. You should see the same trends shown in the plots above.

As always, if you see any issues with any of my results or conclusions above, please let me know! I’m always open to being proven wrong!

Code

I’ve placed the analysis code I used to generate the above plots in the EYFI github repo, which you’re welcome to download and run yourself if you’d like to plug in your own values or just play around with different inputs.

When I get more time, I will also place an embedded Python interpreter here as well, so you can run the analysis directly from this page.

Summer Schedule and Travel

With my son out of school and our extensive summer plans, my time for analysis and posting is pretty low these days, but I’m trying to find time when I can. When my son goes back to school in August, I should have significantly more time for this content. Until then, thanks for your patience!

Heads up that I’m seeing a bunch of broken images.

Dang! You’re right, thanks for the heads up, I’ll investigate.

OK, I think they’re all fixed now. No idea how that happened, I wonder if it’s because it’s so many images. Hopefully it won’t break again. All the more reason for me to try to put all these plots into subplots.

Social Security is “actuarially fair,” so an average person with average health and life expectancy should be indifferent if discounting at a TIPS real interest rate (~2% real). I showed that in my post earlier this year (SWR Series Part 56).

Healthy individuals with a longer life expectancy can push the IRR of delaying benefits to 3% real. That’s a decent IRR for a completely safe “investment” and should not be compared with stock expected returns. A retiree with normal risk tolerance and a balanced portfolio between 60/40 and 80/20 would likely want to delay benefits until age 70 because the IRR of it probably exceeds the expected return of the diversifying asset (bonds).

As you stated in your post, you can justify taking benefits early if you have an extremely high risk tolerance – maybe even risk-neutrality. But I don’t know many people in that category. Maybe celebrity bloggers with enough income from their business who don’t even have to withdraw anything from their portfolio and use the Social Security benefits to invest even more.

So, the real issue for 99.9% of retirees is the tradeoff between hedging your long-term risk (=longevity risk) by claiming benefits at age 70 vs. claiming benefits early and hedging Sequence Risk in the near-to-medium term.

Hey Karsten! Thanks very much for the great info. I can’t think of a better person to critique this post. I may have an academic background, but not in finance/economics like you!

I remember reading that post, and I guess I need to read it again. I’m particularly surprised by your comment “Healthy individuals with a longer life expectancy can push the IRR of delaying benefits to 3% real.” – I need to read your post again to see what I’m missing. Would a longer life expectancy be something like 90+?

Regarding “As you stated in your post, you can justify taking benefits early if you have an extremely high risk tolerance – maybe even risk-neutrality. But I don’t know many people in that category.” I suppose I’m thinking of a retiree that has a few million in the bank by the time they hit their 60’s and thus is quite comfortably FI (which is the case for everyone that has been asking me about this). Wouldn’t this kind of retiree be in that category?

I particularly like your comment about the trade-off between hedging long-term risk vs sequence risk. That would be neat to look at further (unless you’ve already done so).

Thanks again man!

1: In my post, I looked at the tradeoff claiming at age 67 vs. 70. A 67-year-old female with a LE of 21.8 years (age 88.8) could have enjoyed a 3.59% IRR by delaying benefits until age 70. Not bad!

I should also mention that my calculations already factor in the life expectancy, i.e., the discounting is not just the r but also the conditional survival probability.

2: No, that’s not the scenario I thought about. If you’re in your 60s with millions in the bank, you probably withdraw $100k p.a. Then, claiming benefits early, you don’t really invest the extra money. You merely withdraw less. Then this scenario boils down to the tradeoff, as I mentioned: do you reduce Sequence Risk or Longevity risk?

The scenario where you could use the 7% IRR is where your benefits actually create a net investment in the stock market. Not a gross investment that still leaves you with a net withdrawal. And with the net investment, you like to maximize the final expected value, i.e., little or zero risk aversion. Then, sure, go ahead and discount SocSec by 7%. But not many people operate like that.

Hmmm…. you’ve given me a lot to chew on. I think I’ve learned more about the motivation for using the TIPS real interest rate as the discount rate via this conversation than I’ve learned anywhere else. I might end up re-writing much of this post actually.

For example, I can see one mistake I made is using the average American life expectancy from birth, but I should be using the average life expectancy from when you’re in your 60’s. https://www.annuityadvantage.com/resources/life-expectancy-tables/ Blindingly obvious now, ridiculous mistake on my part. Though I’m sure it won’t be my last.

One question comes to mind when considering sequence vs longevity risk: does it make sense to start social security earlier in your 60’s if the market is down heavily? Especially if both equities and bonds are down? That would be neat to analyze.

Unfortunately I’m traveling the next couple weeks, but when I get back I’ll dive into this. Until then, I’m going to put a note at the top of this post to read through our conversation here, at least until I have a chance to reconsider (and likely rewrite) much of the content.

Thanks again!

Thanks for the update.

Regarding the “But I Still Don’t Fully Understand Exactly Why:” Again, an actuary will discount future cash flows with a benchmark rate with similar risk characteristics.

Examples: corporate pension? Use a long-term corporate bond yield! Social Security? Use TIPS yields. A very risky business venture? Likely use a 7% real expected equity return, or likely even more! If 1% seems low, try 1.5%, which is the current long-term TIPS yield.

People may certainly adjust their Stock/Bond allocation in response to higher or lower SocSec benefits because SocSec is clearly a TIPS-like implicit bond holding. But caution: That doesn’t apply to you. Recall that claiming earlier or later makes very little difference in the discounted expected value of SocSec today. You are not changing your implicit bond allocation much, so there shouldn’t be much of an impact on your explicit bond allocation. Example: claiming at age 62, you have expected discounted benefits of $200,000. Claiming at age 70, you expect $210,000. Sure, you can change your bond holdings by $10,000 today due to the new-found bond wealth in your SocSec timing. But not by $200,000!

Glidepaths: Whether or not you claim SocSec early, a GP may partially hedge against Sequence Risk. But notwithstanding what I wrote earlier about the $10,000 difference in expected SocSec benefits, a GP is certainly warranted because as you age, the discounted value of the SocSec benefits declines, and it declines slower for the person who deferred benefits. At age 70, the people who deferred have much higher benefits than those who claimed at age 62. So, if you deferred, you now have a higher implicit bond holding, so you can certainly take that into account in your asset allocation. Deferring benefits, you can afford to let equity weights slide up.

Future work: that all looks good. Looking forward to future discussions!

Best,Karsten (ERN)

I’m going to be a contrarian here.

Let’s consider a hypothetical retiree that’s 62 (with an FRA of 67) with a $2M nest egg, and $6k/mo in spending. If you use the “bucket” method for allocation, that implies $72-216k in cash, $360-576k in bonds/safe divs, and $1.57-1.21M in stocks, giving an allocation between 60/40 and 80/20.

Now if they take a $2k/mo SS payment at 62, then their monthly spending only requires $4k/yr in withdrawals, reducing cash holding to $48-144k and bonds/divs to $240-384k; this means an extra $144-264k can be left in stocks compared to someone who waits until 67. I most certainly think that the extra money in stocks warrants a discount rate higher than the “safe” rate.

Now at 67, the person who waited could be in an even better situation if they had a good market because they may be able to leave even more money invested. But if they had a worse market, they could be in a much worse position because they’ve had to sell while securities were down or flat.

The “safe” discount rate makes sense when you’re comparing a stream of income to cash. But when you’re comparing it to the extra money it allows you to put in the market, the safe discount rate will under-sell the benefit of taking SS early.

For me (probably about 5-7 years from retirement), I plan to decide “on condition” when I will take SS. If there have been some bad market years leading up to the year I turn 62, I’ll take it early. If there have been really strong years, I’ll probably wait. If I wait, I’ll make the decision the next year again based on the market’s condition.

Given that taking SS early allows you to invest more money in the market, I would need to see something more convincing than “use a rate with similar risk characteristics” – the entire power of taking SS early is that it allows you to take more risk with your savings.

Hey Bruce, thanks for stopping by, and for leaving a detailed comment!

It’s been a couple years since I dug into this heavily, and thus had all this info loaded in my brain and had this conversation with Karsten. So I probably could have given you a better response back then, but I’ll give it a go anyways.

Your comment reminds me that I wrote this above: “One question in particular I’d love to analyze: does it make sense to start social security earlier in your 60’s if the market is down heavily? (Especially if both equities and bonds are down?)”

Of course the question is how much is “down enough”? You say you’re going to decide “on condition” when to take SS, but what is that condition exactly?

My suspicion is that this approach requires an underlying assumption of what the market will do in the future, which of course no one knows (especially over a timespan of less than 10 years).

But perhaps we could come up with a metric that works based on historical values. An interesting potential future analysis.

Thanks again!