Last updated: September 8, 2023

- Assumptions

- Median Income Scenario Results

- SocSec Income Vs Retirement Age And Income Results

- Additional Savings Needed to Offset Lost SocSec Income

- Additional Time Needed to Get Savings Needed to Offset Lost SocSec Income

- 1% Real Raise Each Year

- Conclusions

- Code

- Derivation Appendix: Additional Work Time To Offset Lost SocSec Can Be Independent Of Income

Ever since I started diving into social security income analysis, I’ve had one question that kept popping into my head: how will retiring early via FIRE affect your social security (SocSec) income?

This is a site about hitting Financial Independence ASAP after all!

Will you still get SocSec? If so, how much lower will it be? Can you offset that lost income by saving a bit more? How much longer would you need to work to get that needed savings?

Now that I have the tools to compute future SocSec for any scenario, I can finally get some answers!

Now of course if you’re FIRE at an early age, technically you are very unlikely to need ANY social security when you’re older to stay financially solvent. But I think it’s still good to consider what you’re giving up, and how you might take advantage of compounding returns over time to offset that loss if you’d like.

Note: like all my previous analysis, this is primarily a “net present value (NPV)” analysis (essentially considering the time value of money), and does not consider specific market returns other than long term averages. For an analysis that DOES consider various historical market returns in terms of deciding when to start SocSec, see the excellent new article by Big ERN.

Assumptions

As usual, I have to make a number of simplifying assumptions in order to do this analysis. Otherwise the infinite number of possibilities will just overwhelm us.

1. SocSec Rules Stay the Same

There is of course no way to know how the rules and regulations that dictate how SocSec is computed will change in the future.

So, we’re just going to use today’s rules, and assume that they won’t change too much in the future. And if the rules do change, we can just re-run the analysis of course. Given the outrage and political blowback that would happen if benefits are scaled back, I don’t think this is a crazy assumption. We’re also fortunate in the U.S. that we’re not staring down a population aging crisis like other developed countries, due to immigration.

2. All Values In Present-Day Dollars

All input and output dollar amounts are in present-day dollars. So if you find yourself thinking “well what about inflation?”, then remember that we’re keeping everything in today’s dollars so that we don’t have to mentally account for higher prices in the future. SocSec income is of course also adjusted for inflation.

3. Full Retirement Age is 67

For everyone born in 1960 or later, Full Retirement Age (FRA) for social security benefits is 67.

Here in 2023, that means if you’re 63 or younger, your FRA is 67.

For folks born before 1960, the FRA is only a bit earlier (no lower than age 66 if you’re born in the 1950’s).

So given how little the FRA changes for folks born in the 1950’s (someone born in 1953 turns 70 this year, which is the latest age you can start social security), and that everyone born after the 1950’s will have the same FRA, we’ll just use a FRA of 67 in all the analysis below.

4. You Turn 62 in 2023 or Later

I make this assumption for two reasons: 1) so we can use the bend points published for 2023 when computing the Primary Insurance Amount (PIA), and 2) so we don’t have to apply Cost of Living Adjustments (COLA) to the PIA.

Just like for the FRA value above, I strongly suspect that having an earlier birthdate and thus different bend points and COLA on the PIA will not significantly impact the results / conclusions below.

5. You Started Work at Age 22

I just picked age 22 since most folks are graduated from college/university by around then and earning an income. We could easily change this value of course.

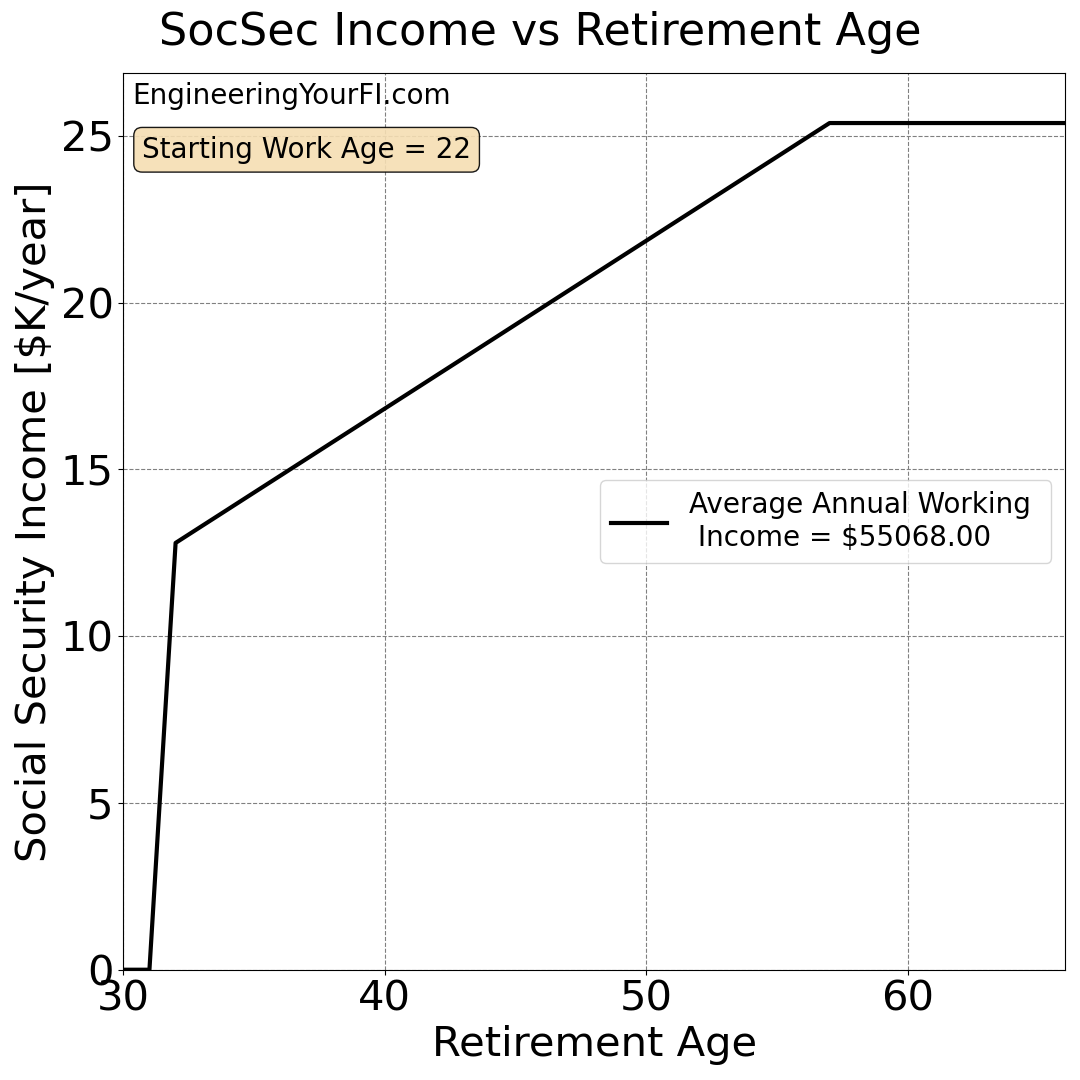

Median Income Scenario Results

Let’s start with a scenario where we assume you have an income equal to the 2022 US median individual income of $55,068 ($1059 weekly) as your average income across your working years.

If you start SocSec at Full Retirement Age of 67, below is the SocSec income you’ll get at age 67 for a range of retirement ages:

If you retire at 40, your annual SocSec income will be $16822.80.

If you instead work until age 57, it’ll be $25381.20/year.

If you instead work until age 67, it’ll STILL be $25381.20/year. Why? Because you already maxed out at age 57 – SocSec is based on the 35 highest earning years, and if you earn about the same amount each year (inflation adjusted), adding more years won’t increase your SocSec income.

That’s why the plot is flat starting at age 57.

So if you retire at age 41 instead of 40, you’ll get $17325.6 – $16822.80 = $502.80 more per year in SocSec income 26 years later, or about 3% more. You can see that slope is pretty consistent from the first age you’re eligible for SocSec (32 in this scenario) until you hit a full 35 years of working history.

SocSec Income Vs Retirement Age And Income Results

Now let’s take a look at a variety of income levels, to see if the SocSec income vs Retirement age relationship significantly changes:

These results make sense: the more you earn, and the longer you work, the higher your SocSec income will be.

We can also now see additional bend points for several of the income levels.

If you have an average income of 40K, the increase in SocSec income is steepest for the first few years after you’re eligible for SocSec (32 to 34), when you’re still fully in the 90% bracket, then it bends down to a lower rate after entering the 32% bracket.

From $50K to $80K, no additional bend points appear from first eligibility to hitting the 35 year work span, staying in the 32% bracket the entire span.

From $90K to $120K, you start in the 32% bracket, but with enough work experience you hit the bend point entering the 15% bracket, which lowers the rate of increase in SocSec income for each additional year of work you do.

Interestingly, even if you’re earning $120K and thus 3x more than someone earning $40K, your SocSec income will still never be larger than about 2x more. Which is due to the brackets described above, which more heavily weight lower incomes.

Overall though, we’re still seeing very consistent slopes for all income levels. There are no really sharp corners in any of the plots except for when you first become eligible for SocSec at 10 years of working (age 32) and when you hit the 35 years of working (age 57).

So that means:

- you should try to get at least 10 years of experience (actually 40 credits, but you can earn a max of 4 credits per year) to be eligible for SocSec before retiring

- if you work beyond 35 years with an income equal to your average income over those 35 years, you won’t be getting any more SocSec unfortunately

And the bulk of the SocSec income is not achieved in the initial 10 years – instead it’s just a steady linear progression from the minimum amount to the maximum amount, roughly doubling the SocSec income from when you’re first eligible (10 years) to the max 35 year mark.

So if you’re thinking about falling victim to the “one more year” syndrome, odds are you’re not going to see a huge increase in your SocSec income by doing so (assuming you’ve become eligible for SocSec). So don’t be afraid to pull the trigger on an early retirement if you’re worried about losing SocSec income.

Additional Savings Needed to Offset Lost SocSec Income

Now what if it still bothers you that you’re going to get a lot less SocSec income than someone who works full time until they reach the traditional retirement age?

What if we save a bit more and take advantage of investment returns over time so that the savings can offset the lower SocSec income by the time we reach traditional retirement age?

How much would that be?

Let’s return to our scenario above where your income is the 2022 US median individual income of $55,068, and assume you retire at age 40 instead of 57 or 67. You’ll get $8,558.40 less per year in SocSec by retiring early.

If you use the 4% rule, that equates to $8,558.40*25 = $213,960 in investments that could provide that same level of income.

So if you retire at age 40, how much more would you need to save by age 40 to have an extra $213,960 in investments by the time you reach age 67?

If you assume a 5% real ROI for your additional savings:

X * (1.05)^(67-40) = $213,960

X = 213960 / (1.05)^(67-40) = $57,308.83

So you need to save a bit over $57K more in your early retirement nest egg to match the SocSec money you’d get later in life (though of course SocSec income is far less volatile, but these are ballpark values anyways – there’s a good chance you’ll end up with far more than an additional $213960 by age 67 as well).

That’s not a trivial amount of money, but if you’ve saved up enough to retire at 40, it’s probably not too tough.

If you assume 7% instead of 5% (invested entirely in equities), then you need to save just another $34432.66.

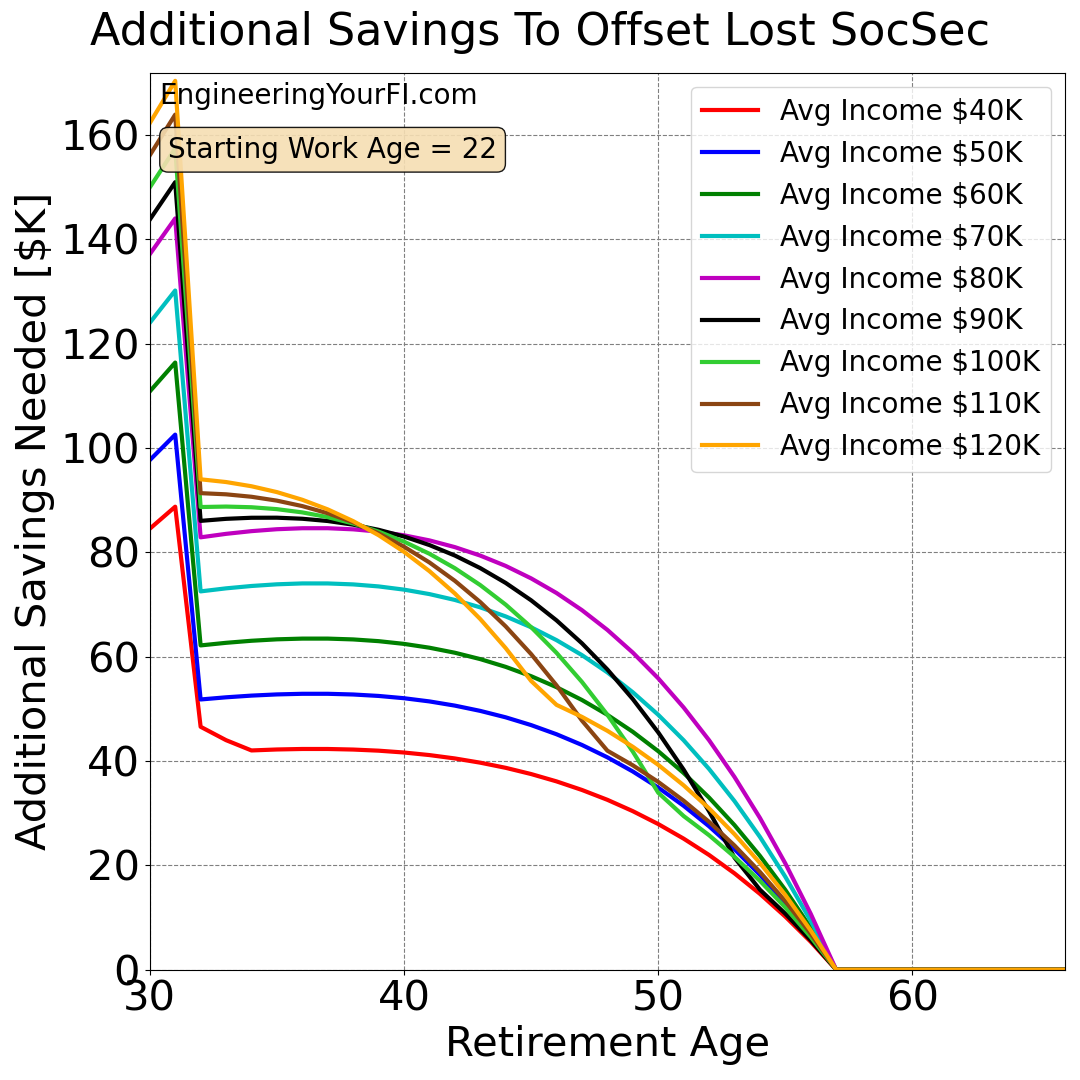

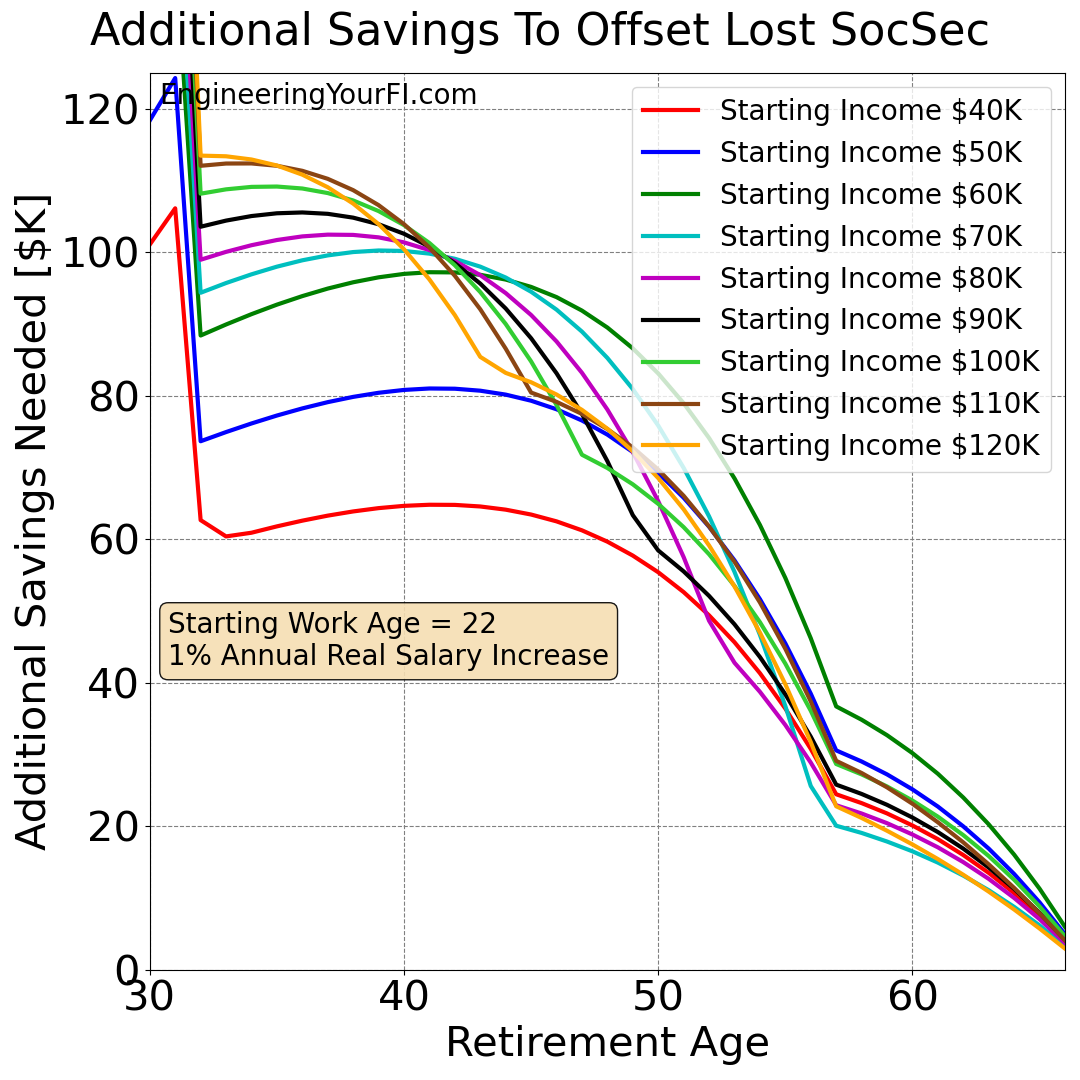

Now let’s look at a wide range of retirement ages and income levels, plotting how much more you’ll need to save by each retirement age to make up for the lost SocSec. We’ll continue to use a 5% ROI.

First off, this is such a beautiful plot! I absolutely love how plots can not only inform decisions, but also just look fantastic. I’m sure everyone on this planet will agree with me.

So let’s unpeel this onion. Lots of things going on and lots of interesting conclusions.

First off, you can see how before you hit SocSec eligibility at age 32, you need a LOT more money saved to offset the entire SocSec income of someone that is eligible for SocSec. Despite the fact that you’d have over 35 years for that amount of money to grow.

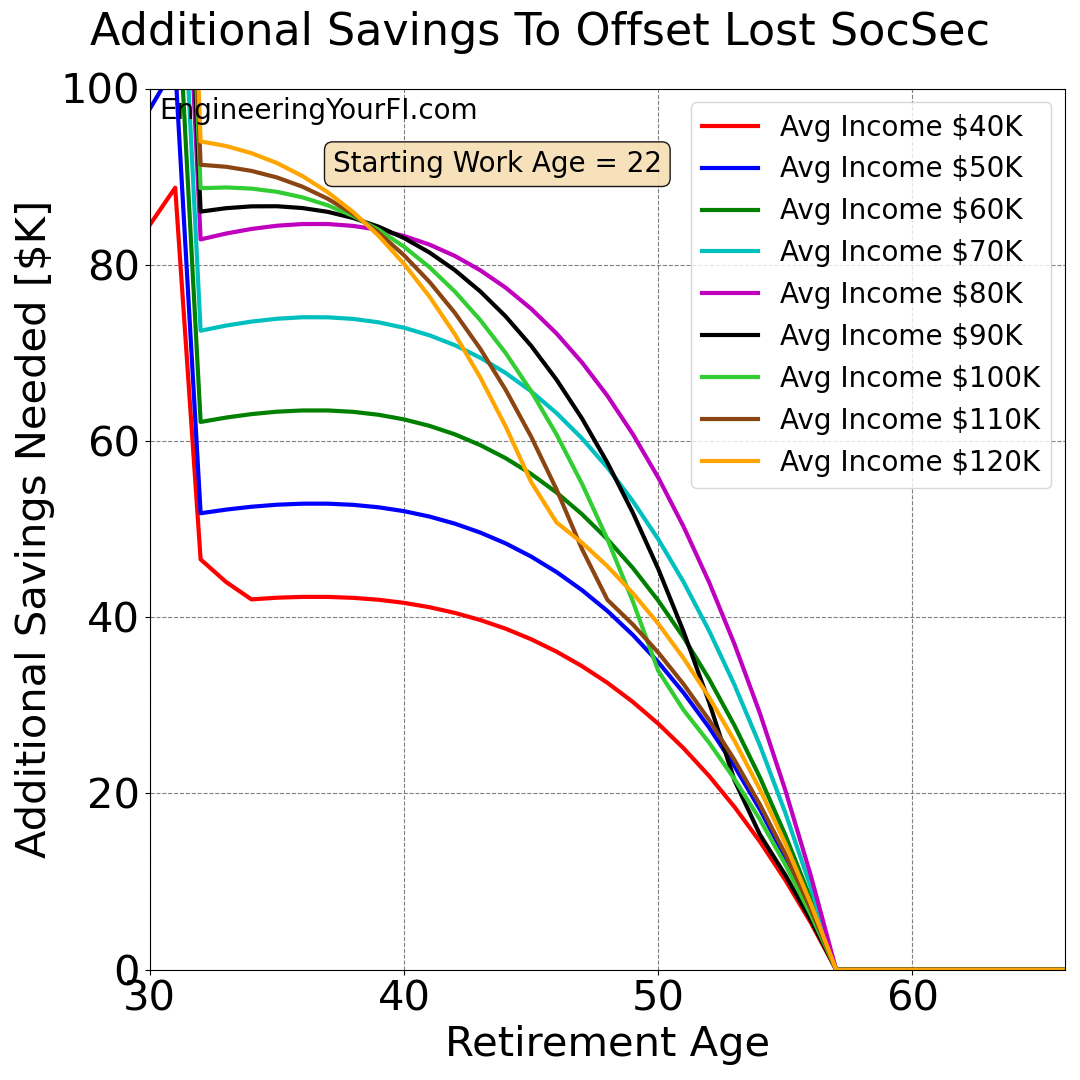

But once you hit that 10 year mark (40 min credits), the amount you need drops dramatically. Let’s zoom in on that region:

Even more beautiful!

You can see how you need less additional savings for the lower income levels, which is logical: those lower income levels will deliver lower SocSec incomes, so you need less savings invested to offset that lost SocSec income.

Now if you look at retirement ages under 40, the lines for incomes under $100K are pretty dang flat. Why?

Because in this range, the additional SocSec you get by working another year is offset by having one less year for your savings to grow (to the needed amount by the traditional retirement age of 67). So the additional amount you need to save to offset lost SocSec doesn’t change much until you’re into your 40’s.

At incomes of $100K or more, the slopes are not very flat at any point, which means every additional year you work will significantly reduce how much money you need to save to offset lost SocSec income.

For all incomes though, as you get into your late 40’s and early 50’s, the lines become quite steep: every additional year you work will significantly reduce how much additional money you must save. Which is logical, as you approach the standard retirement age.

Additional Time Needed to Get Savings Needed to Offset Lost SocSec Income

It’s good to know how much more money you need to offset lost SocSec income, but when you’re at the threshold of FI, TIME starts to become a lot more important.

So I suspect most folks are more interested in knowing how much longer they need to work, versus just how much more money they need.

Let’s once again return to the scenario where your income is the 2022 US median individual income of $55,068, and you retire at age 40. As described above, you’ll get $8,558.40 less per year in SocSec by retiring early, and you’ll need to save an extra $57,308.83 at age 40 to offset that lost SocSec when you hit FRA of 67.

But you don’t have an extra $57K lying around – you just got to standard FI!

So the question is: how long will it take you to save that extra $57K?

First let’s assume you got to FI by age 40 by saving an average of 50% of your income.

If your income is $55068, and you’re saving 50% of that, then you’re looking at $57,308.83 / ($55068/2 per year) = 2.08 years.

BUT: that ignores any growth of the significant assets you’ve saved to achieve FI!

With an annual spend of $55,068 / 2 = $27,534 per year, that means you’ve saved $688,350 to achieve FI (following the 4% rule). If you assume a 5% real ROI on average for your assets, that’s $34,417.50 per year.

So if you’re saving $27,534 per year and your investments are growing $34,417.50 per year, then it will take you:

$57,308.83 / ($27,534 + $34,417.50 per year) = 0.925 years = 11.1 months to get that extra $57K! Less than a year!

And it’s actually even less than that, because you’ll need slightly less extra savings to offset SocSec at age 41 than age 40, but we’ll stick to this “instantaneous” value to keep things simpler (and it’s close enough I think).

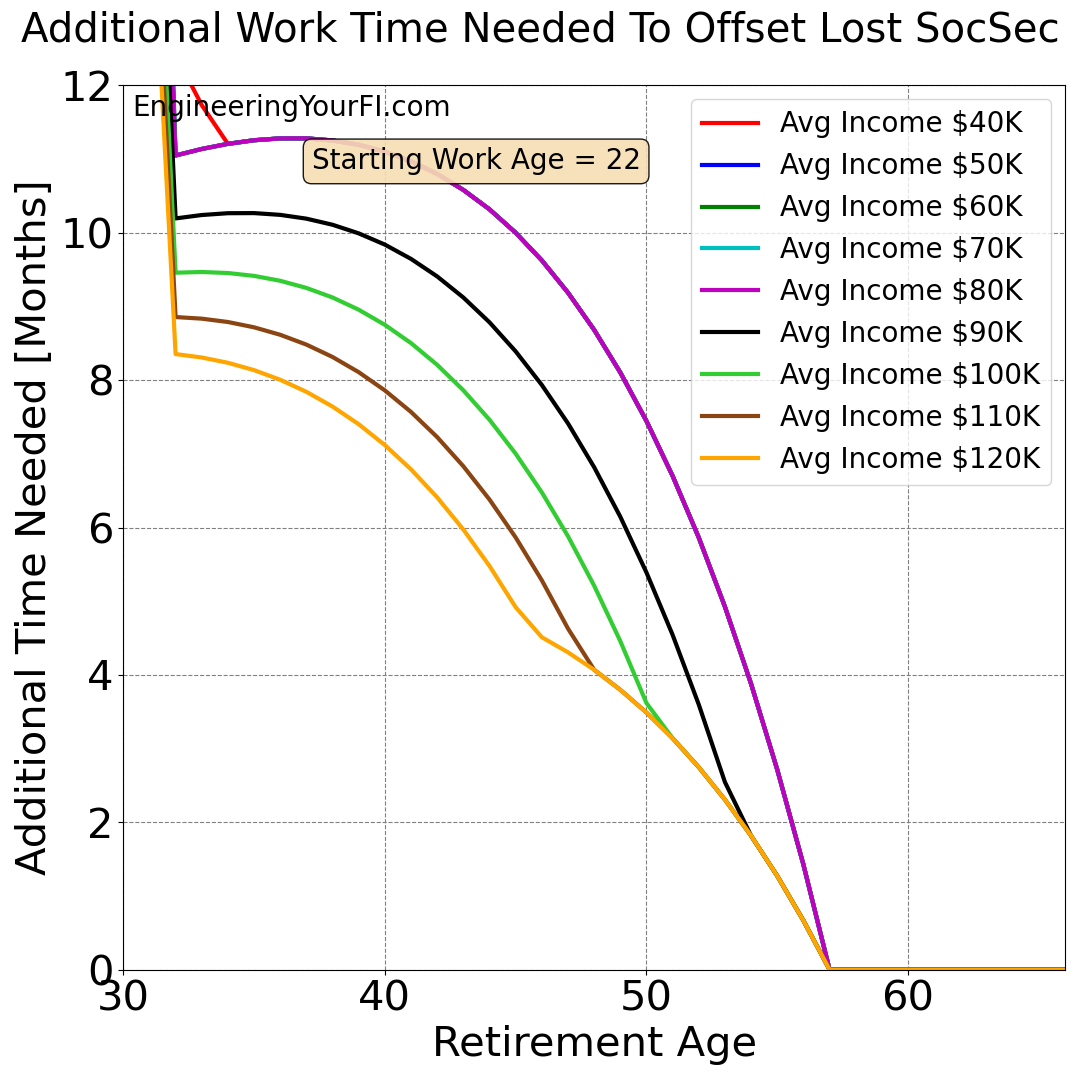

Now let’s compute this time for a wide variety of incomes and retirement ages:

Another very neat plot! And in many ways similar to the plots of required additional savings shown above. Again let’s zoom in, assuming you’ll work until at least you’re eligible for SocSec:

The first thing to point out is that at every income level and retirement age, you’re looking at less than a year of additional saving. Nice!

And the later you retire, the less time is needed to save that extra needed money – which makes sense.

Next, you might have noticed that the lines for incomes $40K to $80K are identical.

And the lines for incomes $90K to $120K eventually merge as well, with later retirement dates.

Why are these lines overlapping?

It turns out that if your average income (over your highest 35 years of earnings) when you retire early (so plenty of zeros in that average) is in the same top PIA bracket as your average income (over your highest 35 years of earnings) with a standard retirement age, the income value itself cancels out of the time computation!

I’ve provided a derivation in the appendix below showing how the income value drops out, see that for the relevant math.

So for incomes $40K to $80K, your top PIA bracket is the 32% bracket for both early retirement and standard retirement (well, the $40K income doesn’t get there until about age 35, as you can see in the short red line in the top left of the plot).

That means regardless of your income in that range, it’ll take the same amount of time to save up the extra money needed to offset lost SocSec income.

For the non-overlapping lines corresponding to incomes $90K to $120K, the early retirement average income is in the 32% bracket and the full retirement average income is in the 15% bracket, which means the income value itself does NOT drop out of the time calculation.

Only when those income lines reach an early retirement age that brings the early retirement into the 15% bracket, does the income value itself drop out of the calculation, and the lines overlap. You can see that happen with each line from $120K at age 45 to $90K at age 55, when the lines clearly change slope to merge onto the “fully top bracket” line.

1% Real Raise Each Year

Everything above assumes a constant average real income level over your entire career. That’s why when you hit age 57 (starting work at age 22), you won’t see any additional SocSec income by working longer, because those extra years won’t bring up your average income at all.

But of course many folks continue to earn increasingly larger incomes as they get older, on top of inflation (so your real income increases).

What if we make the assumption that your income increases by 1% (real) each year, beginning when you start working at age 22?

So if you start earning 40K at age 22, then by the time you hit 67, you’re looking at 40 * (1.01)^(67-22) = $62.59K per year (again, in today’s dollars).

And if by some miracle you start your career at age 22 earning $120K, then by the time you hit 67, you’re looking at 120 * (1.01)^(67-22) = $187.78K per year.

However, not all of that $187.78K will be counted towards social security. In fact, any income above $160,200 as of 2023 is considered beyond the contribution and benefit base, which means two things: 1) you won’t be taxed for SocSec on that additional income, and 2) it won’t raise your average income for computing SocSec either.

If we use the same average income values above as the *starting* incomes instead, I know that both $40K as a minimum and $120K as a maximum are both probably quite high for a typical income span of a 22 year old, but I mainly just want to show how increasing salary over time impacts the results. You can re-run the numbers with smaller starting incomes and a higher rate increase per year if you’d like.

And as mentioned above, once any income reaches $160K, I don’t allow any further increase.

First we’ll re-generate the SocSec income vs Retirement Age and Income plot from above:

This plot isn’t too different than the equivalent constant-income plot above. It just doesn’t plateau, because the increasing salary means that every additional year you work, it replaces your oldest year of work in the 35 highest earning years used to compute SocSec income. Instead it just drops to a lower slope for each income at age 57, when your higher income later years start replacing low income years instead of $0 income years.

Next we’ll regenerate the plot that shows how much more savings are needed at each retirement age to offset lost SocSec income:

You can see how these lines are definitely higher than the equivalent constant-income plot lines above, but not unreasonably so. And the lines no longer go down to $0 at age 57, as expected since you continue to replace lower income years with higher income years.. We do still see a pretty substantial change in the slope at that point though.

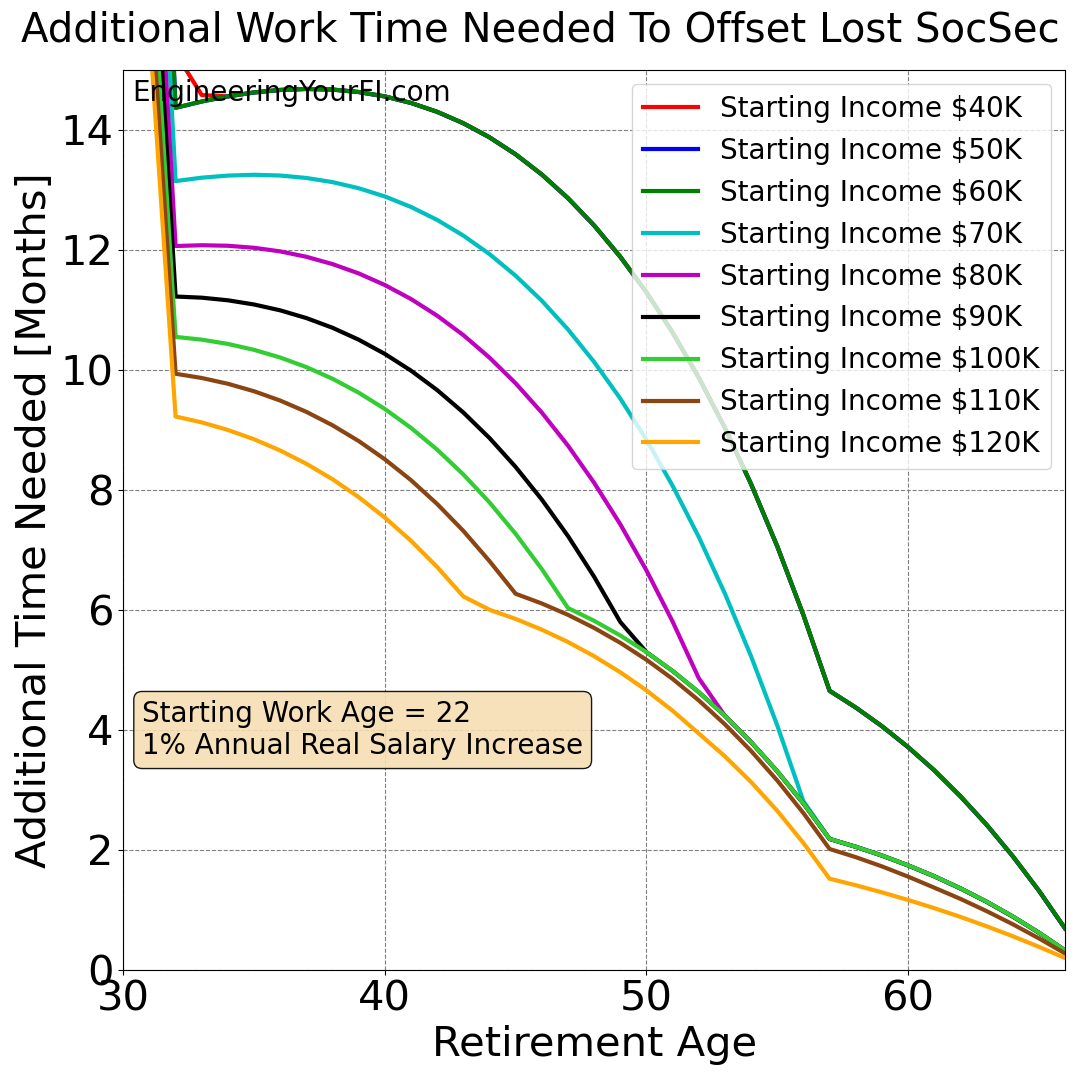

Finally, let’s regenerate the plot showing the additional work time needed to offset lost SocSec income:

Again a bit higher than the equivalent constant-income plot lines above, and again it doesn’t go to zero at age 57, as expected. But again, we’re still in the same ballpark. E.g., for a starting income of $40K to $60K, you’re looking at an extra ~15 months of work to offset the lost SocSec if you retire at age 40, vs an extra ~11 months if your income was constant (in real terms, so just matching inflation). At age 50 it drops below a year of extra work for all income levels.

Conclusions

Overall, I was pretty pleased to see that the impact of retiring early on SocSec income is fairly limited.

And I was even more happy to see that if you’d like to offset that loss of income, you probably won’t have to work much longer to do so. Just work another year or so and you should be set.

Code

I’ve placed the analysis code I used to generate the above plots in the EYFI github repo, which you’re welcome to download and run yourself if you’d like to plug in your own values or just play around with different inputs.

When I get more time, I will also place an embedded Python interpreter here as well, so you can run the analysis directly from this page.

Derivation Appendix: Additional Work Time To Offset Lost SocSec Can Be Independent Of Income

In the “Additional Time Needed to Get Savings Needed to Offset Lost SocSec Income” section above, I discussed how income can actually totally drop out of the time calculation if your early retirement and standard retirement average income are in the same PIA bracket.

Here’s the math behind that amazing result:

AdditionalSavingsTime = AdditionalSavingsNeededAtRetirementAge / AssetIncreasePerYear

= (AdditionalSavingsNeededAtFRA / (1.+ROI)**(FRA – ERA)) / (FIassets*ROI + Income*SavingsRate)

= (AnnualPIAdiff * 25 / (1.+ROI)**(FRA – ERA)) / (FIassets*ROI + Income*SavingsRate)

= ((AnnualPIAifRetireAtFRA – AnnualPIAifRetireEarly) * 25 / (1.+ROI)**(FRA – ERA)) / (FIassets*ROI + Income*SavingsRate)

If both AnnualPIAifRetireAtFRA and AnnualPIAifRetireEarly in the 32% bracket:

= ((AnnualPIAifRetireAtFRA – AnnualPIAifRetireEarly) * 25 / (1.+ROI)**(FRA – ERA)) / (FIassets*ROI + Income*SavingsRate)

= (((0.9 * 1115 + 0.32 * (AIMEforFRA – 1115))*12 – (0.9 * 1115 + 0.32 * (AIMEforERA – 1115))*12) * 25 / (1.+ROI)**(FRA – ERA)) / (FIassets*ROI + Income*SavingsRate)

= (((0.9 * 1115 + 0.32 * (Income / 12 – 1115))*12 – (0.9 * 1115 + 0.32 * (Income * YearsWorked / 35 / 12 – 1115))*12) * 25 / (1.+ROI)**(FRA – ERA)) / (FIassets*ROI + Income*SavingsRate)

And if we assume that your FI assets are 25 times your expenses (equal to Income*(1-SavingsRate)):

= (((0.9 * 1115 + 0.32 * (Income / 12 – 1115))*12 – (0.9 * 1115 + 0.32 * (Income * YearsWorked / 35 / 12 – 1115))*12) * 25 / (1.+ROI)**(FRA – ERA)) / (25*Income*(1-SavingsRate)*ROI + Income*SavingsRate)

Whew, quite an expression! But we now have it down to Income, YearsWorked, FRA (full retirement age, 67 for most folks), ERA (early retirement age chosen), SavingsRate, and ROI.

You can see how the 0.9*1115 and -0.32*1115 terms cancel out – which is vital.

= (((0.32 * (Income / 12))*12 – (0.32 * (Income * YearsWorked / 35 / 12))*12) * 25 / (1.+ROI)**(FRA – ERA)) / (25*Income*(1-SavingsRate)*ROI + Income*SavingsRate)

Then you can see how the income term is now multiplied on every term in the numerator and denominator, so it just cancels out:

AdditionalSavingsTime = (((0.32 * (1 / 12))*12 – (0.32 * (YearsWorked / 35 / 12))*12) * 25 / (1.+ROI)**(FRA – ERA)) / (25*(1-SavingsRate)*ROI + SavingsRate)

Here’s an example where I use an ROI of 5%, retirement age of 40 (which also means 18 years of working if started at age 22), and a savings rate of 50%:

AdditionalSavingsTime = (((0.9 * 1115 + 0.32 * (Inc / 12 – 1115))*12 – (0.9 * 1115 + 0.32 * (Inc * 18 / 35 / 12 – 1115))*12) * 25 / 1.05**(67 – 40)) / ( 25*(Inc*(1-0.5))*0.05 + Inc*0.5)

= (((1003.5 + 0.32 * (Inc / 12) – 356.8)*12 – (1003.5 + 0.32 * (Inc * 18 / 35 / 12) – 356.8)*12) * 25 / 1.05**(67 – 40)) / ( 25*(Inc*(1-0.5))*0.05 + Inc*0.5)

= (((646.7 + 0.32 * (Inc / 12))*12 – (646.7 + 0.32 * (Inc * 18 / 35 / 12))*12) * 25 / 1.05**(67 – 40)) / ( 25*(Inc*(1-0.5))*0.05 + Inc*0.5)

= (((7760.40 + 0.32 * Inc) – (7760.40 + 0.32 * (Inc * 18 / 35))) * 25 / 1.05**(67 – 40)) / ( 25*(Inc*(1-0.5))*0.05 + Inc*0.5)

= ((0.32 * Inc – 0.32 * Inc * 18 / 35) * 25 / 1.05**(67 – 40)) / ( 25*(Inc*(1-0.5))*0.05 + Inc*0.5)

= (0.15542857142857144 * Inc * 25 / 1.05**(67 – 40)) / ( 25*(Inc*(1-0.5))*0.05 + Inc*0.5)

= (1.0407820395437801 * Inc) / ( 25*(Inc*(1-0.5))*0.05 + Inc*0.5)

= (1.0407820395437801 * Inc) / ( 0.625*Inc + Inc*0.5)

= (1.0407820395437801 * Inc) / ( 1.125*Inc)

= 1.0407820395437801 / 1.125

= 0.9251395907 years = 11.1 months

The same nice cancellation of the income happens when your early retirement and standard retirement average income are both in the 15% bracket.

Unfortunately if your early retirement and standard retirement average income are NOT in the same PIA bracket, then you don’t get this nice cancellation.

That’s because the expressions for AnnualPIAifRetireAtFRA and AnnualPIAifRetireEarly have different forms:

AnnualPIAifRetireAtFRA = (0.9 * 1115 + 0.32 * (6721 – 1115) + 0.15 * (AIMEforFRA – 6721))*12

AnnualPIAifRetireEarly = (0.9 * 1115 + 0.32 * (AIMEforERA – 1115))*12

As a result, you’re left with a constant term that does not cancel out.

Let’s see how this plays out if we again use an ROI of 5%, retirement age of 40 (which also means 18 years of working if started at age 22), and a savings rate of 50%:

AdditionalSavingsTime = (((0.9 * 1115 + 0.32 * (6721 – 1115) + 0.15 * (Inc / 12 – 6721))*12 – (0.9 * 1115 + 0.32 * (Inc * 18 / 35 / 12 – 1115))*12) * 25 / 1.05**(67 – 40)) / ( 25*(Inc*(1-0.5))*0.05 + Inc*0.5)

= (((1003.5 + 1793.92 + 0.15 * (Inc / 12) – 1008.15)*12 – (1003.5 + 0.32 * (Inc * 18 / 35 / 12) – 356.8)*12) * 25 / 1.05**(67 – 40)) / (1.125*Inc)

= (((1789.27 + 0.15 * (Inc / 12))*12 – (646.7 + 0.32 * (Inc * 18 / 35 / 12))*12) * 25 / 1.05**(67 – 40)) / (1.125*Inc)

= (((21471.24 + 0.15 * Inc) – (7760.40 + 0.32 * (Inc * 18 / 35))) * 25 / 1.05**(67 – 40)) / (1.125*Inc)

= ((13710.84 + 0.15 * Inc – 0.32 * (Inc * 18 / 35)) * 25 / 1.05**(67 – 40)) / (1.125*Inc)

= ((13710.84 + 0.15 * Inc – 0.32 * (Inc * 18 / 35)) * 6.696207975005938) / (1.125*Inc)

= ((13710.84 + (0.15 – 0.32 * 18 / 35) * Inc) * 6.696207975005938) / (1.125*Inc)

= ((13710.84 – 0.014571428571428569 * Inc) * 6.696207975005938) / (1.125*Inc)

= ( 91810.6361520304 – 0.09757331620722935 * Inc) / (1.125*Inc)

= 81609.45435736036 / Inc – 0.0867318366286483

The answer still depends on Income!