This week I did two main things: create a couple diagrams and fix an acronym mistake.

Doesn’t sound like much, right? How long can it take to put together a couple diagrams and fix a typo? I must be slacking!

Well, turns out those diagrams were some of the most challenging I’ve ever done, and that acronym mistake was spread across lots of posts, diagrams, and plots that I had to recreate. Bleh…

New Retirement Withdrawal Strategy Diagrams

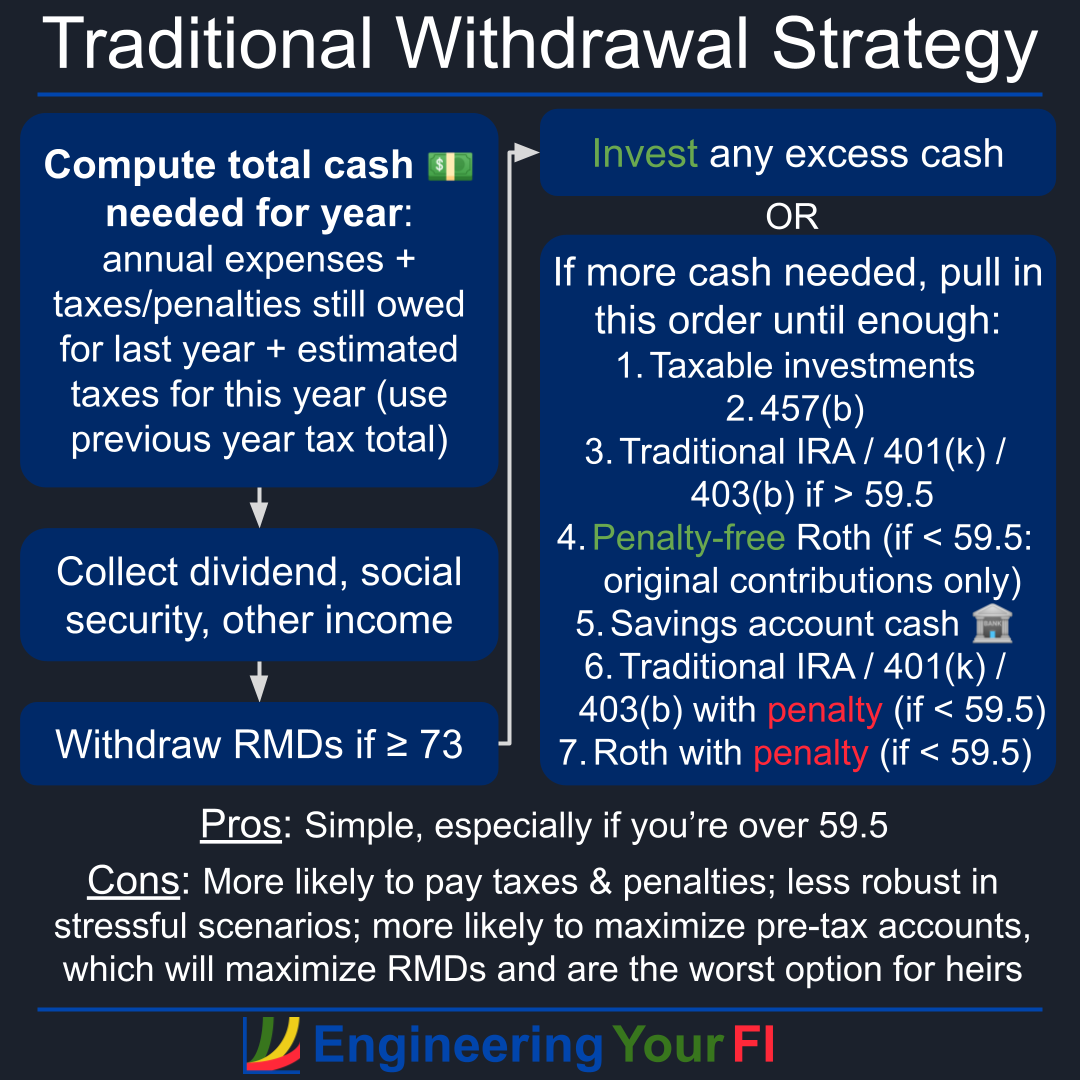

Definitely the more interesting and challenging (and much less annoying) task was creating new diagrams for the Traditional and Tax and Penalty Minimization (TPM) withdrawal strategy pages, which I previously had on the FIRE Withdrawal Strategy Algorithms page.

It was far from trivial getting these full strategies into visual overviews, but I think it’s important to do this work for a couple reasons:

- If someone can start with a 10,000’ overview of the entire strategy, hopefully they can grasp the details much more easily

- By forcing myself to think about what elements of the strategy are important enough to place in the diagram, I gain a much better understanding of the overall process as well, and I can better determine what parts of the strategy are most important to show others

Without further ado, below are the new diagrams for the Traditional and Tax and Penalty Minimization (TPM) withdrawal strategies, which are also now at the top of the pages for each strategy.

Traditional Withdrawal Strategy Diagram

Tax and Penalty Minimization (TPM) Withdrawal Strategy Diagram

Social Security Income Acronym Correction

Creating the new diagrams above was fun and interesting, though definitely also quite challenging.

Discovering that I’d been using a social security acronym for months that stands for something entirely different than I meant: not so much.

Since last August, I’ve been using the acronym SSI for standard Social Security Income. I couldn’t immediately find any standard acronym for this income source, so I thought that I’d just make one up. SSI seemed logical, and something people could easily and quickly grasp.

Well, very unfortunately it turns out that SSI is actually widely known to stand for Supplemental Security Income, which is also provided by the Social Security Administration (SSA). From their site:

“The Supplemental Security Income (SSI) program provides monthly payments to adults and children with a disability or blindness who have income and resources below specific financial limits. SSI payments are also made to people age 65 and older without disabilities who meet the financial qualifications.”

Uhhh…. yeah that’s not at all what I meant by SSI – I was talking about the standard retirement income you get once you reach your 60’s (assuming you’re eligible, as most people are).

CRAP! This meant two things: 1. I needed a different acronym or shorter name for standard social security income, and 2. I had to go back through all the content I’d created using this SSI acronym and fix it – because I really don’t want folks thinking I’m referring to Supplemental Security Income. POOP!

For #1, it took a bit of digging, but I eventually discovered the name and acronym that the SSA uses for standard social security income: retirement insurance benefits (RIB).

I’m guessing it’s not used very commonly, as I found very little content online that uses that name or acronym. Perhaps because RIB doesn’t sound very related to “social security”. But better than nothing I suppose!

So, I then proceeded to correct as much of my old content as practical, starting with the most recent posts and working my way backwards.

Here’s a list of all the posts I updated with this new name, which included updating any diagrams and plots with “SSI” presented in those posts:

- Roth Early Withdrawal Updates and New Withdrawal Strategy Pages

- Status Update: Overhauling the FIRE Withdrawal Strategy Algorithms Page

- Happy Holidays And Farewell 2022

- Stress Testing Analysis Initial Results

- Stress Testing Analysis Update 2

- Stress Testing Analysis Update

- Is It Worth Using Lower Tax Brackets To Reduce RMDs Later?

- Reduce RMDs by Millions And Save BIG in Taxes After FIRE

- The IRS Won’t Wait Forever: Required Minimum Distributions

- How to Pay No Taxes on Social Security Income

- How Much of My Social Security Income Will Be Taxed?

- Withdrawing Money After FIRE

For any old Instagram and Facebook posts that had “SSI” in the diagram or plots, I just added a note at the top of the text description (which you can edit anytime, unlike the graphics). For Twitter, I just added a reply tweet clarifying the meaning of “SSI”.

And finally, for the places in the portfolio projection tool code that used the term SSI, I either replaced that or added a note clarifying its meaning.

Having to comb through all my previous content to fix this mistake was annoying, but it’s also pretty important in my mind – I want to keep all my content as much up to date and clear and correct as possible, so that others can rely on it.

It’s kind of like maintaining an exercise habit – it can be annoying to deal with sometimes, but it’s vitally important.

What’s Next

Well I got one thing done from the “What’s Next” section in last week’s post: New diagrams for the Traditional and Tax and Penalty Minimization (TPM) withdrawal strategy pages.

I’ve also decided to not worry about building a page that describes how the portfolio projection tool I’ve built implements the strategies. The cost/benefit ratio is not favorable – I strongly suspect most folks interested in how the tool works are probably more likely to just review the code itself.

I am still very much interested in creating a new stand-alone TPM withdrawal tool that folks can run for each individual year, rather than a full life-time simulation. This tool will run the TPM method and output exactly how much you should withdraw from each of your accounts during a single year. So hopefully I’ll get to that soon.

Top Tips for Getting To FI and Staying FI

For a while now I’ve been mulling over the idea of creating a “top X tips” list for getting to Financial Independence (FI) (which you’ll find on MANY MANY sites) as well as a “top X tips” list for STAYING FI (which I’m not sure I’ve ever seen anywhere).

In fact, when I google “top tips for staying financially independent”, all I see are lists for how to “become”, “achieve”, “reach”, “gain”, “get closer to” (and many others) FI. Nothing about how to maintain FI.

Ideally I’d like to put these lists in a nice format that folks can easily save/read/share as well. I’ve been thinking about trying Canva for a while, as I’ve heard lots of good things about it from other personal finance creators, so this might be a great way to test it out for the first time.

And if for some reason Canva doesn’t work, especially since there’s not a dedicated Linux app (so I’ll need to use the browser), I might try some alternatives such as Vectr or Penpot Desktop.

Other Future Work

I also still want to do everything I listed in the Future Work section of the post from a couple weeks ago. Lots to do! As always, it’s far easier for me to come up with ideas than to find the time and energy to do them. But I’m still excited about getting to them eventually!